By Michael Roberts

Portugal’s ruling socialists under prime minister, António Costa, achieved a surprising victory in parliamentary elections on Sunday. The Socialists gained an outright majority in the new parliament over all other parties and will be able to rule without a coalition. The previous so-called gerigonca (contraption) coalition broke down last October when the leftist parties (Communists and Left Bloc) left the coalition over what they saw as an austerity budget being proposed by the Socialists.

The Socialist Party wins an outright majority

Costa called a snap election expecting to have to form a new coalition. However, the Socialists took 41.7% of those Portuguese who voted, up 5.4% points from the 2019 election, while the Leftist parties lost 6.9% points. So the total left vote share actually dropped from 52.3% to 50.6%. The main right-wing party, the Social Democratic Party (PSD), did better too, rising from a 27.8% share to 29.3%. But the small ‘centre-right’ parties lost ground, so the Socialist victory was secured.

In effect, there was a consolidation towards the main traditional left and right parties. Except for one thing: there was a sharp rise in the far-right Chega (Enough!) party, which took 7.2% of the vote to become the third largest party in parliament. That’s a sign of things to come if the Socialists cannot deliver on improving living conditions and prospects for the Portuguese people, the poorest in Western Europe.

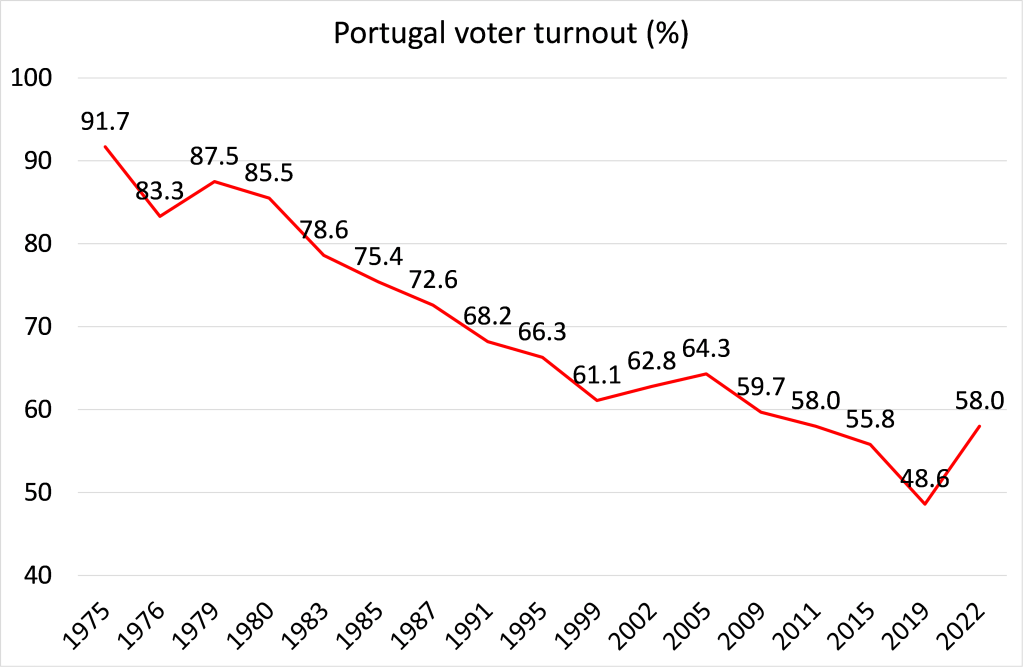

Voter turnout up – but still very low

Voter turnout has been steadily falling since the first democratic election in 1975 after the revolution to overthrow the military dictatorship under Salazar. Then the turnout was 91.7%. In the 2019 election it had fallen to just 48.6%. Sunday’s turnout jumped to 58.0%, the best since 2009. Even so, the ‘no vote’ share of 42% easily outstripped those who voted Socialist (one in five) by some way. Disillusionment in parliamentary democracy remains.

The previous coalition government had supposedly done better than most in response to the pandemic, with one of the highest vaccination rates; but the death rate was still high and only kept within bounds because the Portuguese people showed great solidarity in following restrictions to protect health.

Reliance on tourism

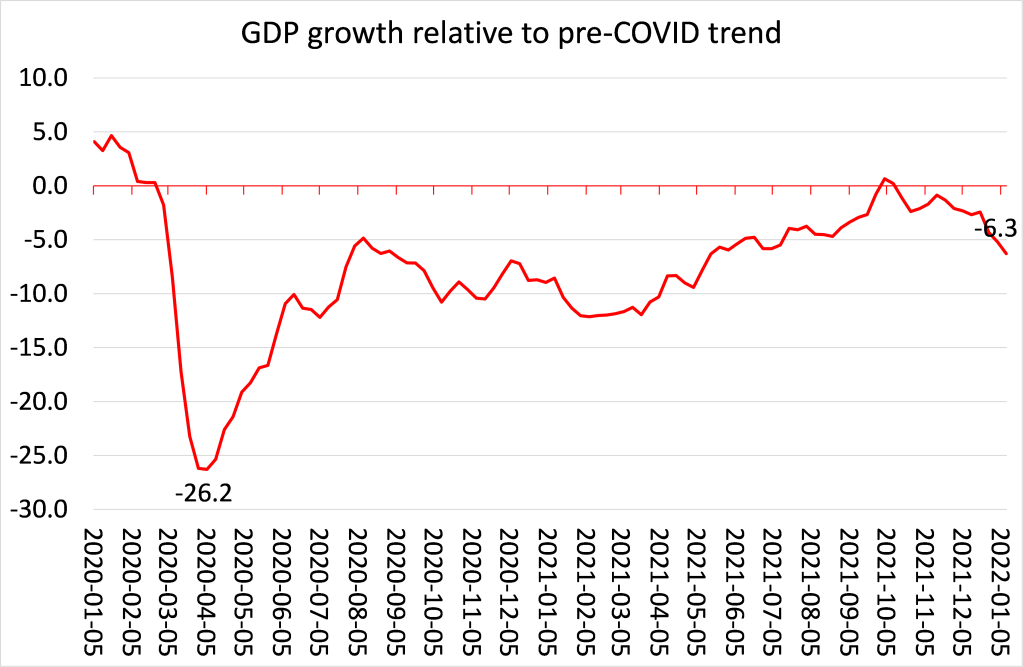

The pandemic was a disaster for an already weak Portuguese economy. Portugal has been called ‘sardine capitalism’ after its famous connection to the production of that fish. But this is misleading: agriculture and fisheries contributes less than 2% of annual GDP and only thousands in employment. Much more important in an economy where manufacturing output and investment is relatively low is tourism. Like Greece, tourism contributes a massive 20% to annual GDP and that has been decimated by the pandemic slump. Portugal’s economy is still well below the trend level before pre-pandemic.

The Costa government came to power pledged to reverse the post 2008 slump austerity policies imposed by the Eurozone. Like other governments in southern Europe in the last decade, it made little progress on growth, productivity and investment, even if it avoided even worse austerity measures. Productivity has been flat for the last eight years.

Productivity level (index = 100)

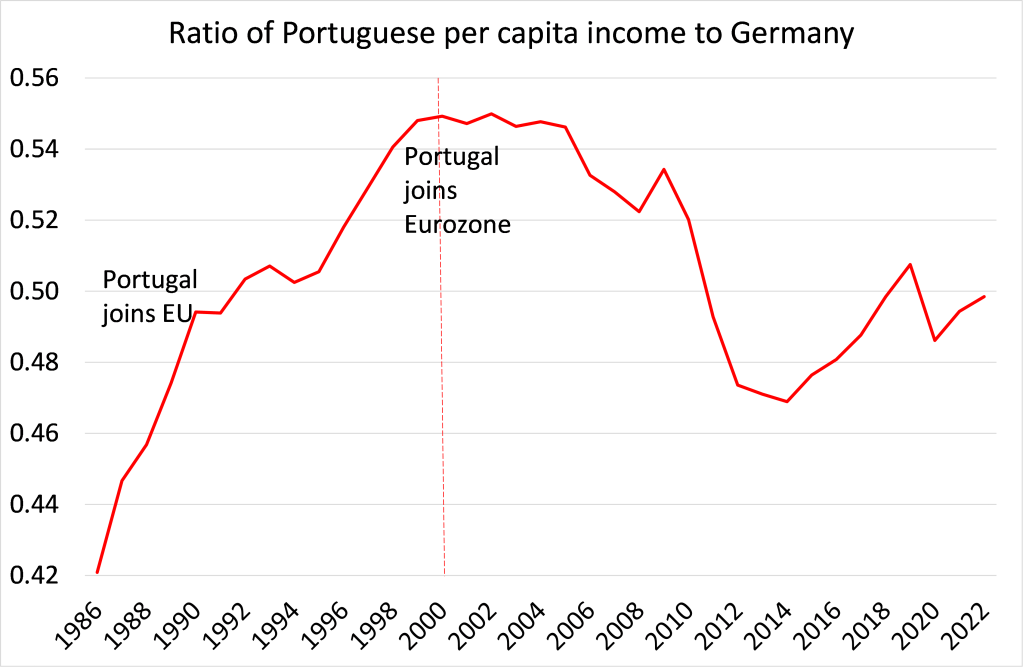

Portugal’s economy has been falling behind the rest of the EU since 2000, when its real annual GDP per capita was 16,230 euros (18,300 US dollars) compared with an EU average of 22,460 (25,330 US dollars). By 2020, Portugal had edged higher to 17,070 euros (19,250 US dollars) while the bloc’s average surged to 26,380 euros (29,750 US dollars).

The European Union supposedly aimed to ‘level up’ the weaker capitalist economies with the richer core. The opening of trade and investment after Portugal became a member in 1986 appeared to work, as it did for other weaker EU countries. But the introduction of the euro changed all that. Whereas before the weaker EU countries could let their currencies depreciate against the Deutschmark to try and remain competitive. That was no longer an option in the Eurozone. Without higher investment and productivity, the weaker capitalist members could not compete. Convergence turned into divergence. Portugal like other weaker members was reliant on foreign direct investment (FDI) from Germany and France. External debt rose sharply and the Euro debt crisis in 2012 in the wake of the global financial crash pushed the country into penury and austerity.

Poor conditions lead to emigration

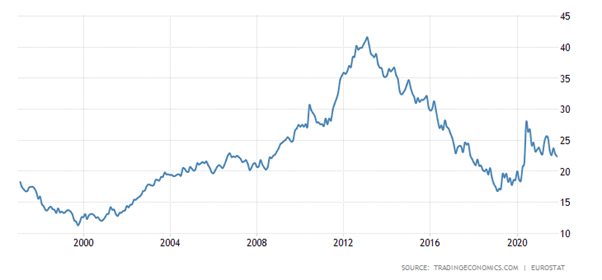

Meanwhile low wages and high unemployment spurred emigration – a feature really since the 1960s. Over the past ten years – a period that includes governments run by both the Socialists and the ‘centre-right’ Social Democrats – some 20,000 Portuguese nurses have gone to work abroad, in an unprecedented drain of medical talent. The youth unemployment rate is still 25%.

Youth unemployment rate (%)

Average pay is just 1,300 euros (1,466 US dollars) a month. Among all OECD countries, Portugal has the sixth-lowest average salary but the highest rise in housing prices. Portugal saw the lowest public investment across the European Union in 2020 and 2021. That was part of the reason the leftist parties pulled out of the coalition.

Banking on the EU post-Covid recovery plan

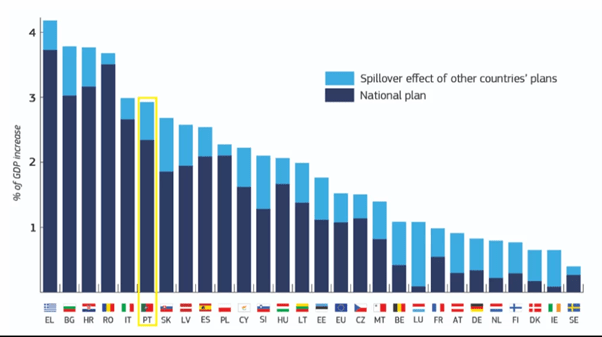

The Socialist government now takes full responsibility for improving conditions for the 99% in Portugal. It is putting all its hopes in the EU’s Recovery and Resilience Plan, which pools funds from the richer members to help out the weaker economies – the first time such a fiscal package has been employed across the EU. The government reckons that the European pandemic recovery plan will have an economic impact of €22 billion ($25 billion) through 2025, and as a result Portugal’s GDP in 2025 will be 3% higher than it would be without that plan.

EU Plan impact

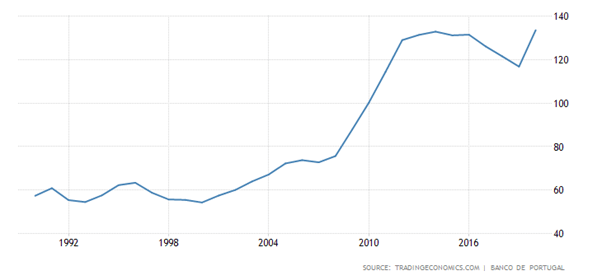

That’s the hope. But the money still comes with strings: namely that the government is supposed to maintain a tight fiscal policy and keep budget deficits down and above all start to reduce its huge public debt ratio.

Public debt to GDP (%)

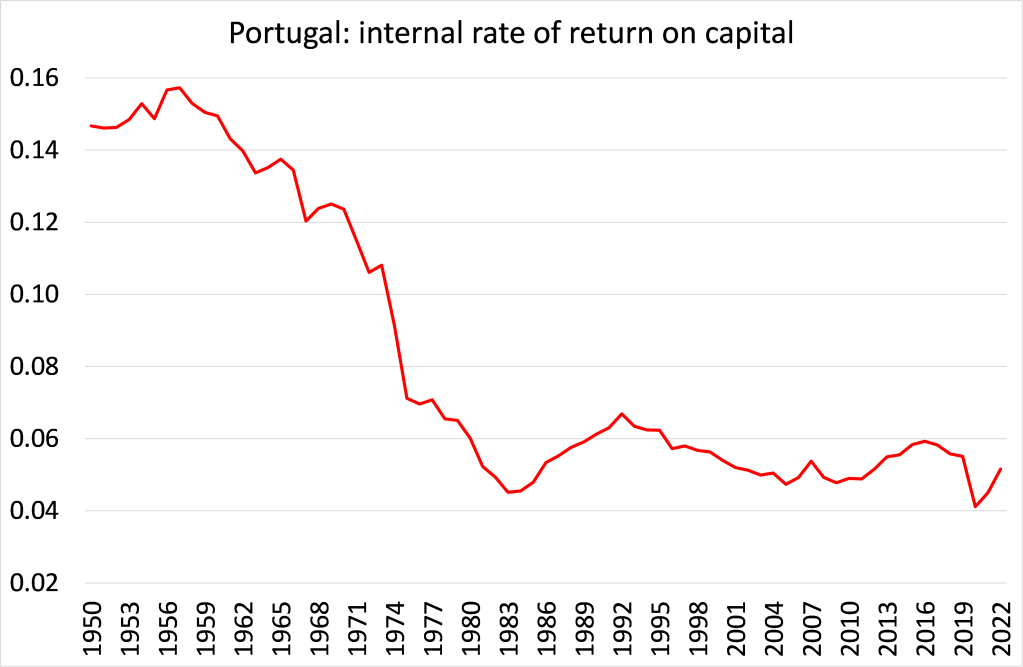

Even though the Socialist government will be getting funds from the EU to spend on infrastructure and services, it is likely to do little to get a very weak capitalist sector to invest and expand employment and raise wages. That’s because the profitability of capital in Portugal is miserable. It has been flat and low for 40 years. The EU has done nothing for Portuguese capital up to now.

Portugal is a tiny country with just 10m population and a $200bn economy. Under capitalism, it is subject to the ‘kindness’ or otherwise of ‘strangers’ (ie German and French capital). And the new Socialist government has no intention of changing that.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.