The scissors of slump

By Michael Roberts

Last week, US Treasury Secretary Janet Yellen told the US Congress that “We now are entering a period of transition from one of historic recovery to one that can be marked by stable and steady growth. Making this shift is a central piece of the President’s plan to get inflation under control without sacrificing the economic gains we’ve made.”

It’s true that the US economy since the depths of the pandemic slump, (which remember in terms of national output, incomes and investment was the worst since the 1930s – even worse that the Great Recession of 2008-9) has made a recovery. But it could hardly be described as ‘historic’. And as for the claim that the US economy, the best performing of the major economies in the last year, is heading towards ‘stable and steady growth’, that is not supported by reality.

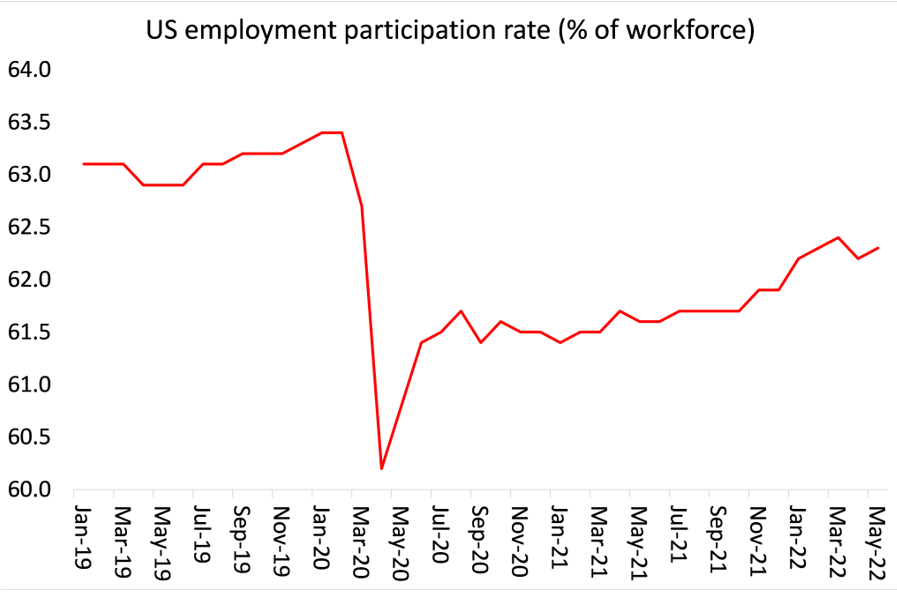

Yes, there is ‘full employment’ of sorts, ie the official unemployment rate is near ‘historic’ lows, but many of these jobs are part-time, temporary or on contracts. And many pay poorly. The employment participation rate, which measures the number of people working out of those of working age, remains well below pre-pandemic levels, levels which were already in decline.

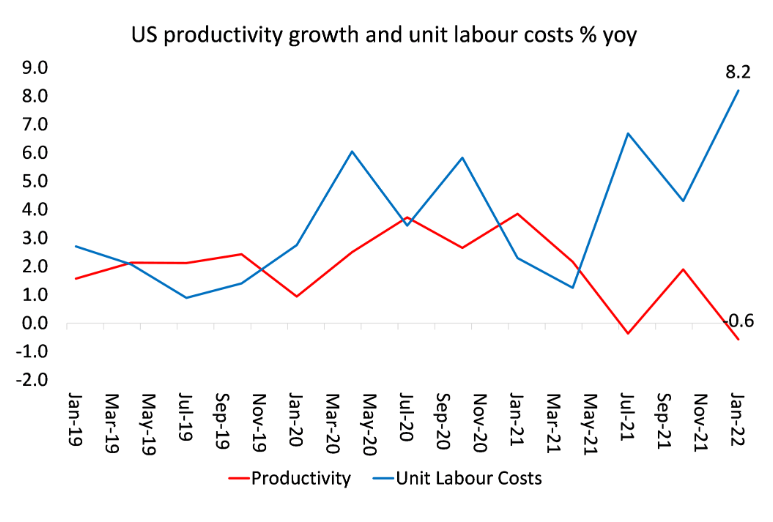

At the same time, productivity growth has been appalling. More Americans have gone back to work since the pandemic but national output is not matching the increase in employment, so productivity per worker has collapsed – from growth rates that were already weak. As a result, unit labour costs (wage costs per unit of output) have shot up, which is shrinking profit margins.

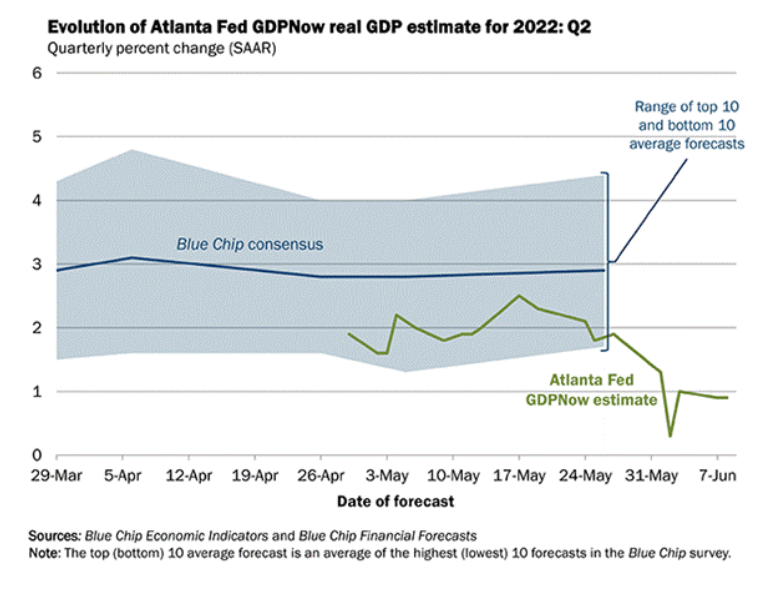

And despite Yellen’s assurances, the prospects for the US economy during the rest of this year and into the next are not promising, even dismal. According to the Atlanta Fed’s GDP forecasting model, the US economy, after contracting in the first quarter of this year, is likely to grow at less than 1% in this current quarter.

Stagflation risks rising as growth slows

Even more contrary to Yellen’s view are the latest reports from the World Bank and OECD economists on prospects for the world economy, including the US. The World Bank’s Global Economic Prospects for June was entitled Stagflation Risk Rises Amid Sharp Slowdown in Growth.

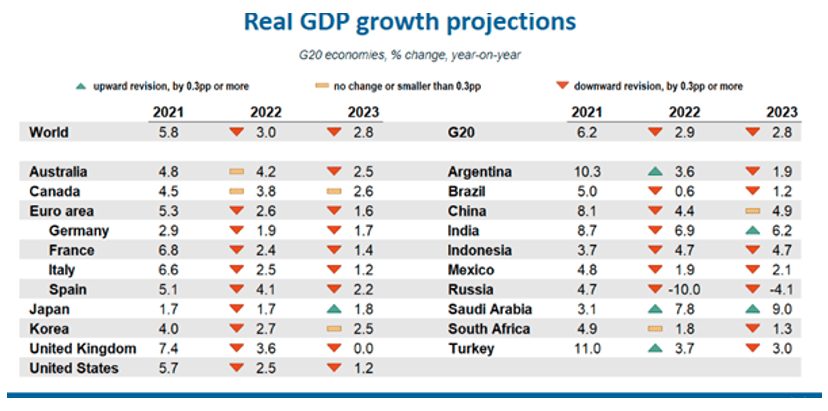

The World Bank economic forecasts were shocking. “Global growth is expected to slump from 5.7 percent in 2021 to 2.9 percent in 2022— significantly lower than 4.1 percent that was anticipated in January. It is expected to hover around that pace over 2023-24, as the war in Ukraine disrupts activity, investment, and trade in the near term, pent-up demand fades, and fiscal and monetary policy accommodation is withdrawn. As a result of the damage from the pandemic and the war, the level of per capita income in developing economies this year will be nearly 5 percent below its pre-pandemic trend.”

Growth in advanced economies is projected to sharply decelerate from 5.1 percent in 2021 to 2.6 percent in 2022—1.2 percentage point below projections in January. Growth is expected to further moderate to 2.2 percent in 2023, largely reflecting the further unwinding of the fiscal and monetary policy support provided during the pandemic. Among emerging market and developing economies, growth is also projected to fall from 6.6 percent in 2021 to 3.4 percent in 2022—well below the annual average of 4.8 percent over 2011-2019.

“The negative spill-overs from the war will more than offset any near-term boost to some commodity exporters from higher energy prices. Forecasts for 2022 growth have been revised down in nearly 70 percent of EMDEs, including most commodity importing countries as well as four-fifths of low-income countries.” So the World Bank forecasts stagnation in output with inflation still present.

Eurozone growth predicted to be below USA

As for the US, the World Bank forecasts just 2.5% growth in national output this year, 2.4% in 2023 and then just 2% in 2024 – a ‘stable and steady’ growth, you might say, but only at the low levels that the US economy has experienced in the long depression since 2009. And the US performance is forecast to be the best among the advanced capitalist economies: the Eurozone area will manage only 1.9% by 2024 and Japan just 0.6%.

World Bank economists reckon that the combined impact of the pandemic and the war would leave global economic output in the five years from 2020 to 2024 more than 20 percent below the level implied by trend growth between 2010 and 2019. The impact on poor countries will be much greater with developing economies a third less than expected and output in commodity-importing developing countries — especially badly hit by the sharp rise in food and fuel prices provoked by Russia’s invasion — more than 40 per cent less than expected!

The view of the OECD economists is, if anything, even more pessimistic. In June’s Economic Outlook, called The Price of War. OECD economists emphasise the cost of the Russia-Ukraine war. “The world is paying a heavy price for Russia’s war in Ukraine. It is a humanitarian disaster, killing thousands and forcing millions from their homes. The war has also triggered a cost-of-living crisis, affecting people worldwide. When coupled with China’s zero-COVID policy, the war has set the global economy on a course of slower growth and rising inflation – a situation not seen since the 1970s. Rising inflation, largely driven by steep increases in the price of energy and food, is causing hardship for low-income people and raising serious food security risks in the world’s poorest economies.”

Global GDP growth is now projected to slow sharply this year to around 3%. This is well below the pace of recovery projected last December. Growth is set to be markedly weaker than expected in almost all economies. Many of the hardest-hit countries are in Europe, which is highly exposed to the war through energy imports and refugee flows. Global growth will slow further to 2.8% in 2023 – that’s near ‘stall speed’, with the UK having no growth at all, the worst result in the G20 (apart from Russia). Even the US will slow to just 1.2%.

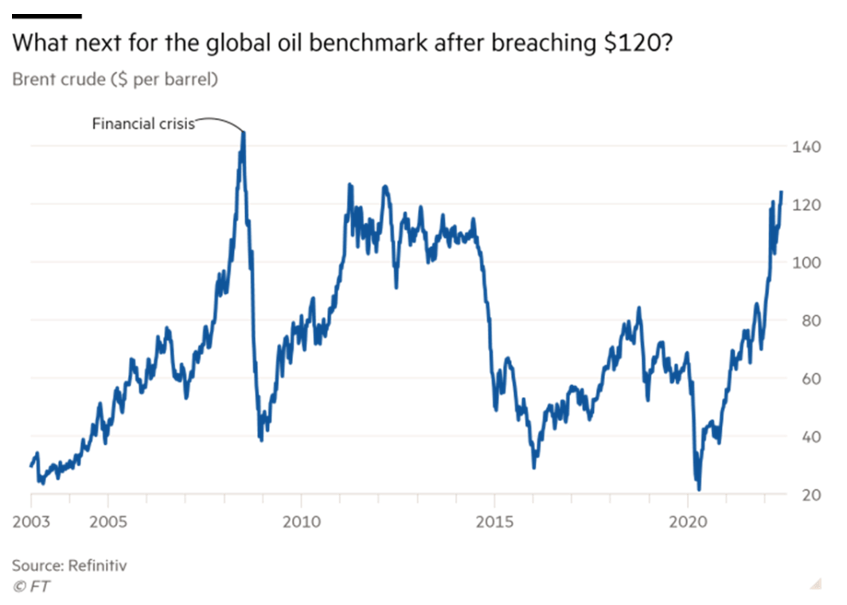

Crude oil prices might reach $150 a barrel

And inflation of the prices of goods and services in the major economies does not look like abating during the rest of this year. Crude oil prices could go even higher than the current $120/b. Jeremy Weir, chief executive of the commodity trade Trafigura, said that energy markets were in a “critical” state as sanctions on Russia’s oil exports following its invasion of Ukraine had exacerbated already tight supplies created by years of underinvestment. “We have got a critical situation. I really think we have a problem for the next six months . . . once it gets to these parabolic states, markets can move and they can spike quite a lot.”

A parabolic move in markets is generally defined as when a price that has been rising suddenly surges to hitherto unseen levels, mimicking the right side of a parabolic curve. Weir added it was highly probable that oil prices could rise to $150 a barrel or higher in the coming months, with supply chains strained as Russia tries to redirect its oil exports away from Europe.

Energy prices are not rising because of ‘excessive demand’ or even because of ‘price-gouging’, but simply because supply is being restricted. Supply dropped during the pandemic and now Russian exports are sanctioned and cannot be replaced by Saudi oil or US supply.

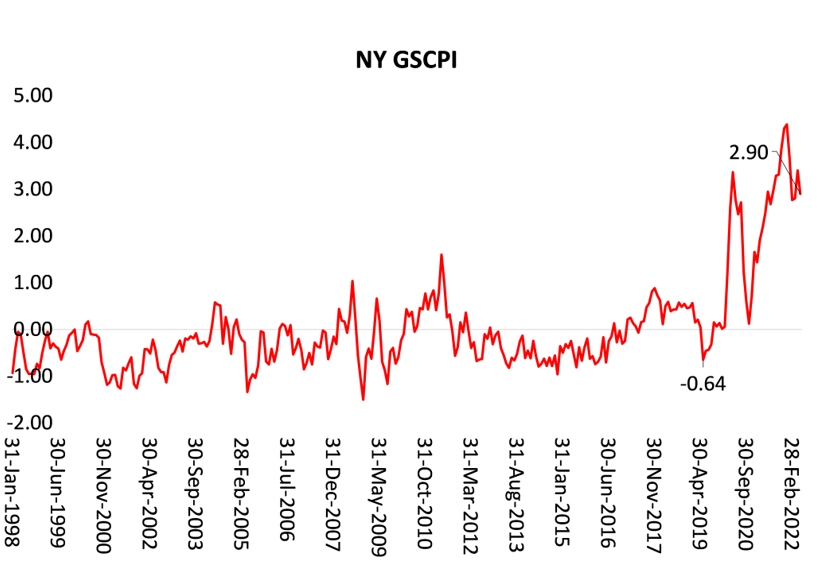

The global supply chain breakdown since the pandemic continues, particularly since the start of the Russia-Ukraine conflict but even before – see the NY Fed measure of supply squeeze below.

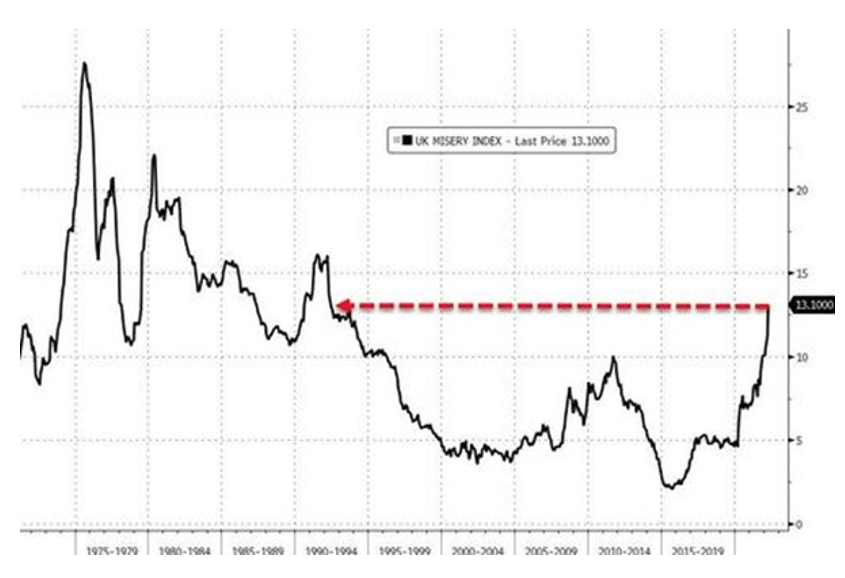

Of the major economies, the UK is set for highest inflation among G7 until 2024 and the lowest growth. A combination of higher energy prices, a slumping pound, faltering economic growth, a deteriorating environment for small businesses, weak households, trade restrictions on Russia, a central bank that is tightening, and overall inflation at four-decade highs have all produced a toxic environment for the UK economy. The so-called ‘misery index’ which measures the unemployment rate plus the inflation rate as an indicator of ‘misery’ for working-class households, is heading back towards levels not seen since the Thatcher era.

Sharp fall in real incomes

The nexus between rising prices and wages has led to sharp fall in real incomes as a result. Price rises are outstripping wage growth nearly everywhere and households are seeing a loss of disposable income (ie after price rises and taxes) and so are forced to run down savings (some of which was built up during the pandemic lockdowns) to make ends meet.

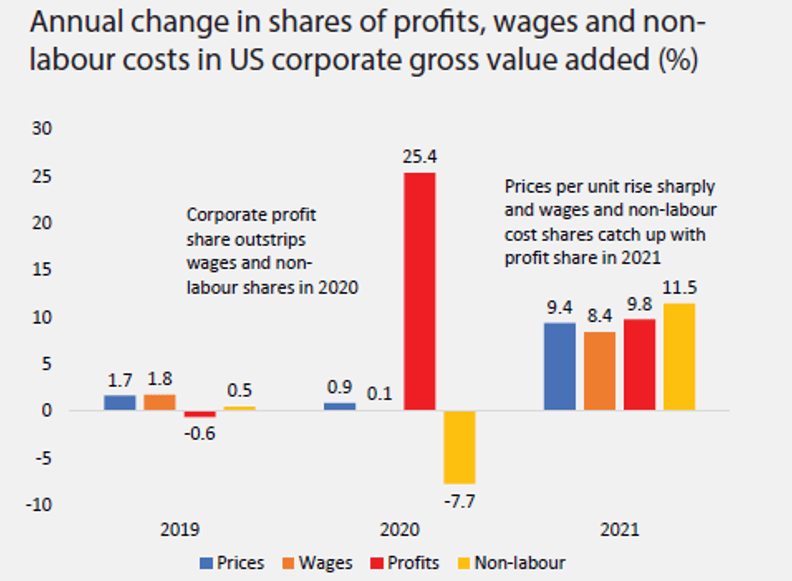

As I have shown before in previous posts in some detail, that, contrary to claims by mainstream politicians, central bank governors and economists, there is no ‘wage-price’ spiral. Wages are not driving prices up. Indeed, it’s profits that have risen sharply as a share of value since the pandemic. However, rising unit labour costs (as shown above) because of low productivity growth, are beginning to eat into profit margins.

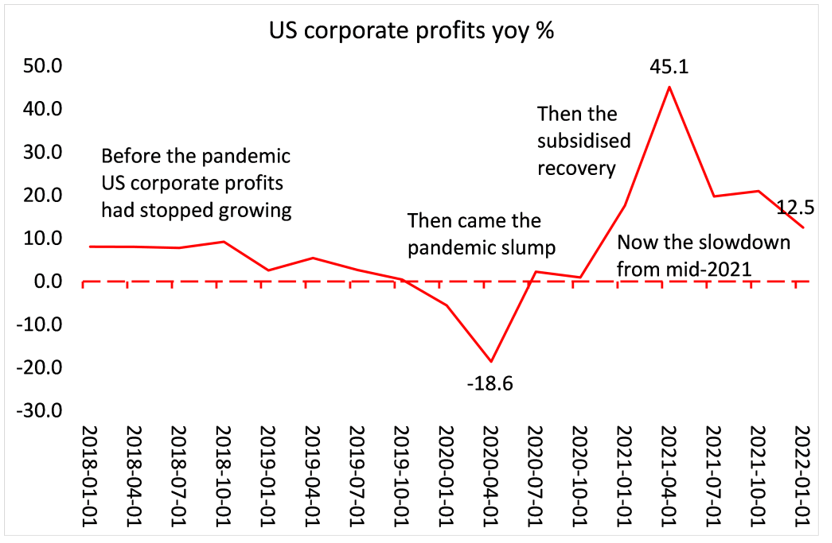

Falling profit margins will eventually lead to lower profitability and even a falling mass of profit. That would be the signal for a new slump, especially if the costs of borrowing to invest rise as central banks hike interest rates in a vain attempt to ‘control’ inflation. Falling profits is the formula for an eventual investment and production slump. That’s one blade of the scissors of slump.

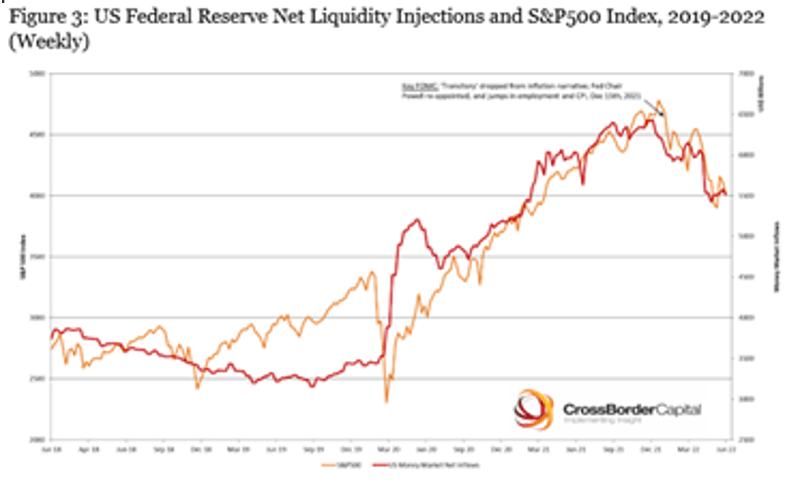

The other blade is debt. As I have outlined on many occasions, I reckon this next major slump will be triggered by a corporate debt meltdown. In particular, remember the size of what are called ‘zombie companies’ that do not get enough profit to cover even their debt servicing commitments; and ‘fallen angels’, those companies which have borrowed too much to invest in risky assets that now face blowing up. And corporations that are debt-loaded are heading for trouble as borrowing costs rise and banks tighten liquidity. Already the Federal Reserve has raised its policy rate and moved from ‘quantitative easing’ to ‘quantitative tightening’, taking stock market prices down as a result.

The World Bank economists are worried. “The faster-than-expected tightening of financial conditions worldwide could push countries into the kind of debt crisis we saw in the 1980s. That is a real threat and something we are worried about. Even quite small increases in borrowing costs will be a problem,” said Franziska Ohnsorge, a lead author of World Bank report.

Central banks are raising interest rates rapidly

World Bank data show that foreign debt in low-income countries rose by $15.5bn to about $166bn in 2020. Foreign debt in middle-income countries rose by $423bn to more than $8.5tn, leaving them especially exposed to interest-rate rises. Central banks are raising rates rapidly in the most widespread tightening of monetary policy for more than two decades. Over the three months to the end of May, monetary authorities announced more than 60 rate rises. More are expected in the months ahead.

Any downturn in profits and rise in borrowing will expose the layers of businesses that are close to going bust. In the UK, Financial Stability Board chairman Martin McTague, commented “there is still a massive problem with small businesses. They are facing something like twice the rate of inflation for their production prices and it’s a ticking timebomb. They have got literally weeks left before they run out of cash and that will mean hundreds of thousands of businesses, and lots of people losing their jobs.”

McTague referred to the Office for National Statistics (ONS) data, showing that 2 million (or about 40%) of the UK’s small businesses had less than three months of cash in reserves to support operations. He noted that 10% (or 200,000) were in grave danger, and 300,000 only had a few weeks of cash left. “It is a very real possibility because … they don’t have the cash reserves. They don’t have any way they can tackle this problem.”

A ’Ponzi’ scheme that will face a reckoning

In Europe, its largest financial asset manager has likened parts of the private equity industry to a “Ponzi scheme” that will face a reckoning soon. “Some parts of private equity look like a pyramid scheme in a way,” Amundi Asset Management’s chief investment officer Vincent Mortier said. “You know you can sell [assets] to another private equity firm for 20 or 30 times earnings. That’s why you can talk about a Ponzi. It’s a circular thing.”

In other words, private equity companies are buying up companies with huge loans and then selling them onto each other using even bigger loans. Eventually, somebody will lose out from this ‘pass the parcel’ form of finance. Leverage (borrowing) levels have increased proportionately, with debt levels reaching an all-time high.

The scissor blades between falling profitability and rising debt costs are closing and will eventually cut investment, jobs, prices and wages.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.