[Editorial Note: although this is a much longer read than most Left Horizons articles, we are publishing here the full text of the report produced last week by Unite the union, on corporate profiteering in the UK]

Across the economy, profiteering has fuelled the cost-of-living crisis.

Rampant corporate profiteering has fuelled the cost-of-living crisis. As the pandemic eased in 2021, many companies managed to push up their prices and profits. Corporate profiteering – not workers’ wages – has helped drive inflation “spirals”. And even as the economy now heads towards recession, many companies, in many industries, continue to make high profits.

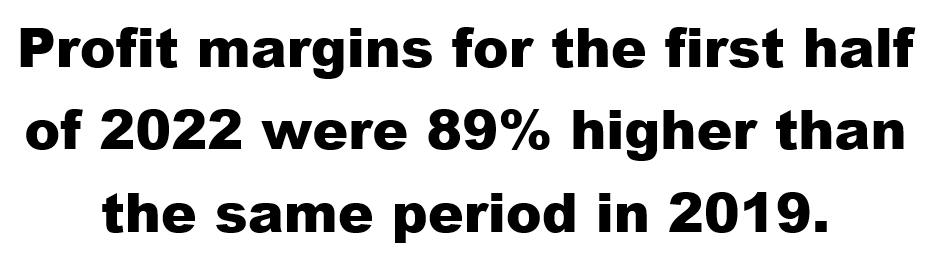

Unite’s first profiteering report, published in July 2022, showed how 2021 profit margins of the FTSE 350 (the UK’s biggest listed companies) jumped 73% compared to 2019. Our new research, using the latest available company figures, shows how profits spiked even more after that. Profit margins for the first half of 2022 were 89% higher than the same period in 2019.

This new report doesn’t just present the latest evidence for overall profiteering. It digs deeper to explain how this has been happening across the economy.

The effects of sky-high profits are well known in energy, where oil and gas companies, and electricity generators, have made windfalls as household fuel bills shoot up. The government’s current windfall taxes on energy profits, full of get-out clauses, just tinker at the edges. But energy is only a part of the story.

Profiteering has been happening in many industries. We follow the supply chains of key goods which are together responsible for the majority of overall inflation. We see how companies from supermarkets to shipping tycoons, car dealers to food manufacturers and agribusiness giants, have been cashing in on drought, war, and post-pandemic demand to push prices and profits through the roof.

It has been happening across different kinds of markets: in government-licensed monopolies, in cartel-dominated industries, and in “competitive” markets too.

The crisis is systemic: corporations and investors, facilitated by governments, have won enormous power to set the rules and reap the rewards. Their economy is failing the vast majority of us, both as workers and consumers.

Profit margins jumped in 2021 – and even more in the first half of 2022.

Unite’s first report on profiteering, published in June 2021, showed how many companies pushed up their profits at the end of the pandemic. Profit margins of the UK’s big listed companies – the FTSE 350 – jumped 73% higher in 2021 than they had been in 2019.

Our new report shows this profiteering continued, and spiked even higher, last year. We have now analysed FTSE 350 company profits for the first half of 2022. (The large majority of companies have not yet published full year profit figures for 2022.) The jump is even bigger: profit margins for this period were 89% higher than before the pandemic in the first half of 2019.

Profit-price spirals: deep dive on key goods and their supply chains

The initial triggers of inflation were “supply shocks” including climate crises, post-pandemic bottlenecks, and more recently the Ukraine war. But many companies have taken advantage to boost their profits, driving up prices even further.

This report investigates where and how profiteering has caused “spiralling” inflation. It looks at three key types of goods suffering some of the biggest price rises: energy (domestic electricity and gas); food; and motoring expenditure (petrol and automobiles).

We have chosen these three Office for National Statistics (ONS) “categories” for three reasons. They have seen some of the highest price rises and are together responsible for the majority – 57% – of overall inflation (See Section 3.1). They play key roles in the broader UK economy. And also, they include industries where many Unite members work.

We map the supply chains of these goods to identify just where price rises are hitting, and how companies are profiting from them. We then zoom in on key transport industries – road freight, ports, and shipping – which are central to many of them.

The profiteering crisis is already well known in energy. According to leaked Treasury forecasts, UK gas producers and electricity generators could make “excess” profits of up to £170 billion over two years. Our own research in this report shows how the world’s top 10 oil giants pocketed £174.5 billion between them just in 2021; the UK’s Big Four energy generation and supply companies took £9.5 billion; and the gas and electricity distribution monopolies £6.3 billion. These are the mouths we feed with our fuel bills.

But the issue goes well beyond energy. It runs right through the economy.

It’s happening close to home. Big supermarket chains, and other retailers such as car dealerships, are boosting profits by increasing their prices even more than rising supply costs. For example, Tesco, Sainsbury’s and Asda – the top three supermarkets – doubled their combined profits to £3.2 billion in 2021 compared to 2019. Big brand food manufacturers have also boosted their profits.

It’s visible deep in global trade networks. The four global giant agribusiness corporations (ADM, Bunge, Cargill and Louis Dreyfus), which dominate crucial crops such as grains, saw profit shoot up 255%, making a combined $10.4 billion in 2021. The world’s top ten semiconductor manufacturers made £44 billion between them – 96% more than in 2019.

It has been particularly glaring in crucial transport industries. The UK, highly dependent on imported goods, is hard-hit by price rises from the giant container shipping multinationals. Eight top shippers including Maersk, COSCO and Hapag-Lloyd made a combined £62 billion in 2021 – boosting their profits by an incredible 20,650% on 2019 (i.e., 200 times higher). Port owners such as DP World and CK Hutchinson have also seen big gains. The profits of the biggest road freight operators were up 149%.

Together, the goods we look at in this report are responsible for 57% of overall inflation; and for each of them there is evidence of runaway profiteering across the supply chain. That is to say, the majority of inflation is being driven by industries where profiteering is rampant. The cost-of-living crisis is a profiteering crisis.

The economy isn’t working: how markets systematically fail workers and consumers

Reading business and general media, it’s common to hear company bosses worrying that a looming recession will push their profits down. That could yet happen. But so far, many companies, particularly big corporations, have been doing very well indeed. This report uses a wealth of industry-level evidence to look at just where that profiteering has been happening. It also gives a deeper economic analysis, to look at just how it happens.

Economic analysis: Five channels of profiteering

“Free market” economic theory says that prices and profits should come down as firms compete and undercut each other. But across a whole range of markets, this has been failing to happen. The broken economy provides plenty of opportunities for firms to profiteer – that is, take advantage of a crisis.

Specifically, we identify five main economic channels of profiteering:

Supply crunch. After a supply chain shock, demand chases reduced supply – this allows companies to push up prices and profits. (Examples: food crops hit by widespread droughts; semiconductors hit by pandemic production halt, raw material shortages and trade wars.)

Demand jump. An increase in demand for a good, while supply remains constrained, allows companies to lift prices. (Examples: many consumer products at the end of the pandemic.)

Market windfall. Centralised market pricing structures help companies score “windfall” profits – where a market-wide price jumps due to factors unrelated to many companies’ costs. (Examples: oil and gas, wholesale electricity market.)

Market concentration (oligopoly). Where a few large companies dominate an industry, they can have greater power to increase mark-ups. (E.g., oil and gas, shipping, ports, supermarkets.)

State-licensed monopolies. In some key industries, companies are granted government concessions which give them major power to set prices, encouraged by failing regulation. (E.g., North Sea oil fields, electricity and gas distribution networks, other privatised utilities.)

These channels often overlap. Underlying many of them is tacit collusion by companies to set prices high above costs. (We look in depth at these points, and the underlying economic theory, in Section 4 of the full report.)

Who’s responsible?

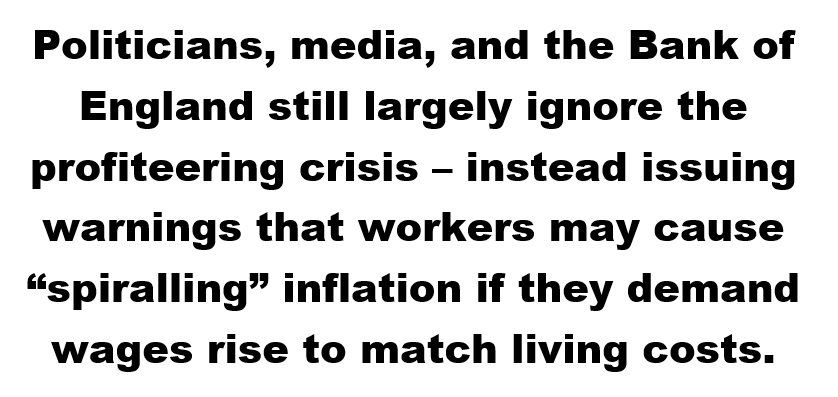

Politicians, media, and the Bank of England still largely ignore the profiteering crisis – instead issuing warnings that workers may cause “spiralling” inflation if they demand wages rise to match living costs. But this narrative flies in the face of reality: real wages have seen their biggest falls in decades.

It also contradicts what firms themselves are saying. In a survey from March 2022, 56% of US retailers said inflation had allowed them to raise prices beyond what was required to offset increased costs, with 63% of large businesses reporting they were using inflation to boost profits. BP’s chief executive has said his business is a “cash machine”, while BMW’s chief financial officer talks about “a significant improvement in pricing power.” When they tell us they are ripping us off, we should listen.

Politicians try to shift the blame onto workers, while tinkering with minimal answers like an oil and gas windfall tax that is full of get-out clauses. But this report shows how the problem is systemic. Profiteering is rife both in “competitive markets” and where there is government regulation. Across a range of industries and markets, bosses and investors have been reaping gains from crisis – while the economy systematically fails the vast majority of us, both as workers and as consumers.

Petrol

Petrol prices climbed to record levels over 190p per litre in July 2022, and have remained much higher than long-term averages. Looking closer, prices have jumped all along the supply chain: from global crude oil, to the spreads charged by refineries, to the final mark-up at the pumps. And at every step, big profits are being made.

The top 10 global oil companies made £174.5 billion between them in 2021 – up 37% on 2019. Nine of the top 10 UK North Sea producers have published their 2021 global profits: they made a combined £41.4 billion in 2021, up 50% on 2019.

Oil and gas production is dominated by a mixture of state-owned giants (e.g., Saudi Aramco and PetroChina) and privately owned multinationals (e.g., BP and Shell). These companies have benefited from windfall profits so large that BP’s CEO described the company as a “cash machine”.

And their profits are set to be even higher for 2022. The five oil majors which have already posted 2022 figures recorded net profit of £124.2 billion in 2022 – an increase of 271% compared to 2019. As US President Joe Biden commented in July 2022 about one of these companies, ExxonMobil: “Exxon made more money than God this year.”

Britain’s six petrol refineries are reported to be making more money “than they have ever witnessed”, with the BBC reporting that profits per barrel jumped by 366% in the year to June 2022.

Just six refineries control the bulk of the UK’s petrol supply. Half are owned by US multinationals such as Valero and Exxon Mobil, and one is owned by a joint venture between billionaire Jim Ratcliffe’s Ineos and the Chinese government. While refining capacity has remained stable, the margin refiners make on wholesale petrol tripled in 2022 – from around 10p to up to 35p per litre added on petrol prices. The indications are that this has dramatically boosted profits. ExxonMobil’s CEO has described the current context as a “very, very high margin environment”, while industry analysts say “the refiners are printing money at the moment.”

Petrol retailers made £1.3 billion profit between 2016 and 2020. Profits are likely to have risen even further since, due to record prices of over 190p per litre.

Petrol retailing is dominated by the big supermarkets, with the brands of oil multinationals also taking a large share. Because supermarkets do not break down their profits for petrol retail from other income, it is harder to identify profiteering here. But the RAC argues that supermarkets and other retailers have used price rises to make an extra £7 million a month in profit. Our analysis estimates that Tesco, Sainsbury’s and Morrisons would have made a combined £323 million on fuel sales in 2021-22. Profits are likely to have improved further in 2022 as the gap between wholesale and retail prices has increased.

Energy

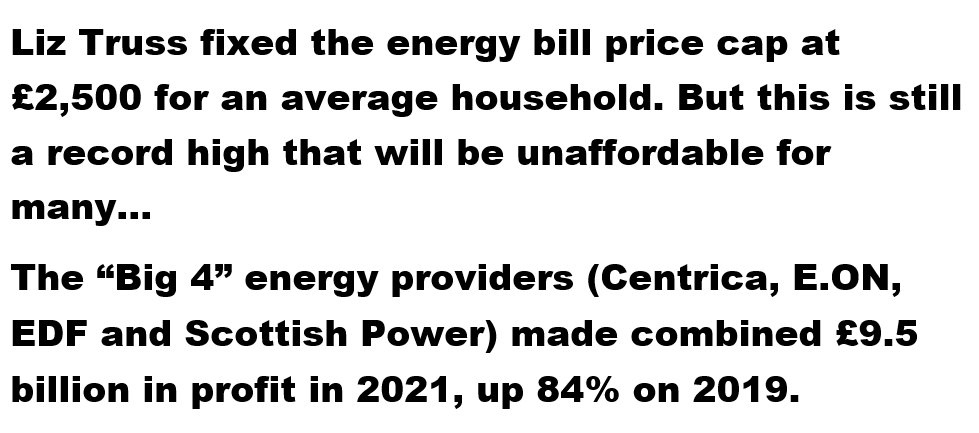

Household energy bills have hit record levels. Responding to massive public pressure, former Prime Minister Liz Truss fixed the energy bill price cap at £2,500 for an average household. But this is still a record high that will be unaffordable for many.

One big driver is wholesale energy prices. The price that generation companies charge for supplying electricity to the grid jumped nearly five times over 2021, triggered largely by a spike in natural gas prices. That has meant windfall profits for gas suppliers and many generators. But the energy distribution networks, and the biggest retailers, are also cashing in.

The “Big 4” energy providers (Centrica, E.ON, EDF and Scottish Power) made combined £9.5 billion in profit in 2021, up 84% on 2019.

Some smaller suppliers have gone bust due to cost increases. But the big four energy companies, which are all active in electricity generation as well as retail gas and electricity supply, are profitable and have increased their market share.

Their profit bonanza is set to be even bigger in 2022. Centrica, the owner of British Gas, reported a record-high operating profit of £3.3 billion for 2022. Earlier in the year, they reinstated a dividend worth £59 million. The company’s CEO, Chris O’Shea, said it was “the most challenging energy crisis in living memory” – but apparently not for Centrica’s shareholders.

E.ON, meanwhile, posted profits of €2.5 billion in the first half of 2022. Earlier in the year, the company’s CEO, Michael Lewis, warned that consumers would have to cope with extraordinarily high fuel bills for at least 18 months – presumably to ensure that the company’s dividend payments, announced in the same month, could continue.

A small number of private companies have been given licensed monopolies to run the electricity and gas distribution systems. These are effectively state-licensed cash machines – the electricity and gas distributors made a combined £6.3 billion in 2021, and both have ongoing operating margins over 40%.

National Grid plc has a monopoly to run national electricity and gas transmission networks, while regional distribution grids are run by a small number of private companies. Their prices are supposedly controlled by regulator Ofgem – yet, according to analysis by Common Wealth, the gas and electricity distribution operators have been making long-term operating profit margins of over 40%.

Our analysis shows they had an even better year than usual in 2021 – with the gas and electricity distributors recording combined profits of £6.3 billion. The companies pocketing this money include UK Power Networks, owned by CK Group, the company of Hong Kong’s richest billionaire Li Ka-shing; and Northern Powergrid, owned by US billionaire Warren Buffet’s Berkshire Hathaway conglomerate.

UK generators have already made more than £10 billion in “excess profits” due to spiking electricity prices, according to the Treasury.

The wholesale electricity price – the rate at which generators sell their energy to the grid – jumped nearly 5 times higher in 2021. This was triggered by increased gas costs: yet gas is responsible for less than 40% of electricity generation, meaning that other generators had a “windfall” as their sales price rose high above costs. UK Treasury officials estimated in May 2022 that UK electricity generators could have made more than £10 billion in “excess profits” by that point.

But this could be just the start. According to Bloomberg, the Treasury currently forecasts that UK gas producers and electricity generators could make “excess” profits of up to £170 billion in the next two years.

Food

There have been huge increases in the costs of food staples in the UK and worldwide. The initial causes were widespread droughts and other climate disasters, compounded by jumps in fuel and other input costs, and most recently the Ukraine war. But all this has been made worse by profiteering along global supply chains – from agribusiness multinationals to high street supermarkets.

Tesco, Sainsbury’s and Asda – the top 3 supermarkets – nearly doubled their combined profits to £3.2 billion in 2021 compared to 2019.

The food retail sector is highly concentrated: the top three companies, Tesco, Sainsbury’s and Asda control 56% of market share. Despite the rise in wholesale prices, these companies increased their profits by 97% in 2021 compared to 2019. Tesco is also ramping up shareholder pay-outs. The company paid out £704 million in dividends in 2021-22 and commenced an enormous share buyback scheme in July 2022 intended to return over £1 billion to shareholders by April 2023.

Supplying the supermarkets are the food manufacturers. They are also enjoying good times: 8 top UK manufacturers made profits of £22.9 billion in 2021 – with both profits and margins up 21% on 2019.

While the situation has been described as “extremely challenging” for the food sector, that doesn’t seem to apply to the top UK food manufacturers or their parent companies: healthy profits are being made. Eight of the top UK food manufacturers made a combined total of £22.9 billion in 2021. The biggest winner was Nestle, which alone pocketed net profit of £13.7 billion – up by nearly £4 billion on 2019. The good times for the company have continued into 2022, in no small part thanks to steep price increases.

The four dominant agribusiness conglomerates (Archer-Daniels-Midland, Bunge, Cargill and Louis Dreyfus) have “cashed in” on food price jumps to increase profits by 255% in 2021 compared to 2019.

Four giant multinationals – known collectively as “ABCD” – play a key role in trading global food commodities. These companies posted combined profits of $10.4 billion in 2021, up 255% on 2019. Their combined profit margin was also up 173% in the same period. Business media have noted that these companies are “reaping big gains” and have “cashed in on booming agricultural markets”.

In 2021, the parent companies of the four main UK fertiliser producers increased their profits by 23% in comparison to 2019 – even while blaming “soaring energy costs” for factory closures and job cuts.

Fertiliser, one of the key inputs to agriculture production, has soared in price since 2021. The parent companies of the top 4 UK fertiliser producers made combined profits of $1.4 billion in 2021, a 23% increase on 2019.

Automotive

A shortage of new cars has seen consumers turning to the second-hand market. UK dealerships have taken advantage of this by boosting the prices of second-hand cars – and their profits. At the other end of the supply chain, suppliers of key components, notably semiconductors, have also seen big profits. And in the middle, car manufacturers are making record gains.

Major car dealerships saw a 110% rise in profits and a doubling of profit margins between 2019 and 2021. At the same time, the largest dealerships shed thousands of jobs and pocketed millions in government furlough support.

The drop in new car production has resulted in a surge in second-hand demand; dealers have taken advantage by increasing prices, with family-friendly models in particular jumping in price between 50% and 60%. We have profit figures for 65 of the top 100 UK automotive retail groups: their combined 2021 net profit was £1.1 billion, up 110% on 2019, with margins doubling. The five largest UK dealerships (including Sytner, Arnold Clark and Lookers) received a total of £257 million in government assistance in 2020-21 and slashed a combined 7,410 jobs.

The top car manufacturers with UK operations have also managed to get in on the profits bonanza – recording a combined net profit of £45 billion in 2021, up 134% compared to 2019, with margins increasing by 128%.

As with the prices of used cars, the prices of new cars have increased dramatically. While the chief executive of the Society of Motor Manufacturers and Traders (SMMT) described the situation as “challenging”, many car manufacturers have turned a healthy profit. And the good times have continued into 2022: BMW announced that it had posted net profits of €13.2bn the first half of the year alone, while Stellantis recorded half-year profits of €8.0bn in 2022. This hasn’t fed through into improved conditions for workers, however, as BMW staff face falling earnings and plant closures.

The top ten global semiconductor companies have used a surge in demand to make a combined £44 billion profit in 2021, up 96% compared to 2019.

The US-China and Korea-Japan trade wars, as well as halts in production caused by Covid-19 and natural disasters, have resulted in semiconductor demand outstripping supply. Semiconductor companies have been able to leverage this situation to nearly double 2021 profits versus 2019. The largest semiconductor manufacturer, TSMC – which has over 50% of the global market share – announced that its net profit figure had surpassed the NT$1 trillion (equivalent to US$33 billion) mark for the first time, up by more than 70% from a year earlier.

Road freight

Issues in the UK road freight industry – particularly a shortage of drivers – have been well covered in the media. Other problems include increased fuel and vehicle costs. Our analysis of company profits, however, shows that freight companies have largely managed to pass on costs related to these issues, boosting profit margins.

The combined profit margin of the UK’s major road freight companies has jumped 67% on 2019 levels.

79 of the biggest 100 road freight operators have reported their profits for 2021. Their combined net profit margin has gone up to 4.2%, from 2.5% in 2019.

The parent companies of top road freight operators increased their profits by 149% compared to 2019.

Together, nine of the biggest UK road freight operators– Wincanton, Turners and Royal Mail, along with the global logistics giants Deutsche Post (DHL), FedEx, XPO, Kuehne + Nagel, La Poste (DPD) and UPS – made £21.1 billion in 2021, up from £8.5 billion in 2019, with profit margins increasing by 90%.

Ports

The UK is the most expensive cargo shipping destination in Europe, with a standard 20ft container costing nearly 25% more to ship from Shanghai to the UK than to continental Europe.

The UK’s ports are dominated by six companies. Four of these have published 2021 accounts, showing double-digit profit margins.

ABP Ports, the UK’s largest port operator, made £126 million net profit in 2021 with a margin of 21.8%. Peel Ports made £143 million with a similarly high margin of 24%. DP World, notorious for its illegal firing of P&O workers, made £863 million globally – a mere 10.8% margin. And CK Hutchison’s global ports division reported operating profits of over £1 billion – on a 25.4% operating margin.

Profitable UK port operators are nevertheless set to receive millions in government support as part of the Freeport scheme, including at least £50 million going to DP World.

Other profitable operators like Hutchison Ports will also benefit from government support.

Container shipping

Probably the most blatant example of inflation profiteering is container shipping – an industry which is particularly crucial to the UK due to its status as an island nation with a large trade deficit in goods. This industry is dominated by a handful of multinational giants, who have joined together in three alliances that control nearly 85% of world container trade. This massive market power is helping shipping companies take advantage of the post-pandemic demand surge to accumulate eye-watering profits.

Eight of the top 10 global container shipping companies had reported 2021 profits at the time of writing. Their combined total was £62 billion in 2021 – up an astonishing 20,650% on 2019. On the back of this, they paid out £4.7 billion in dividends last year. These already record profits are set to be smashed in 2022 as the container lines are forecast to make a staggering £212 billion.

While shipping companies have faced increased transport expenses, these appear to be far below the freight price increases they’ve introduced. Recent reports suggest they will continue to enjoy phenomenal profits in 2022. According to Bloomberg, profits are expected to reach $256 billion (£212.2 billion) in 2022 results.

The US, UK, Canadian, Australian and New Zealand competition authorities are coordinating investigations of suspected anticompetitive conduct by shipping companies. The companies have been accused of “blatant profiteering” and potential “cartel activity”.

Five international government authorities are now probing anticompetitive practices in the industry. Australian Competition and Consumer Commission chairman, Rod Sims, has argued that legal exemptions may allow freight companies to “get together and engage in cartel activity”. In June 2022, US President Joe Biden passed the Ocean Reform Act, which gives the US Federal Maritime Commission to intervene into shipping fees. International freight forwarding bodies have argued the companies have engaged in “blatant profiteering”.

[Note: This is the full text of the summary of the report published by the trade union UNITE, on profiteering in the British economy, in, March 2023. There were 72 endnotes and references at the end of the summary and they have been removed from this version of the summary for brevity. However, the original summary with all endnotes, (or the full report) can be found here.]