By Michael Roberts

This blog was originally published by Michael Roberts last Friday, 5 May 2023. The original article can be found here.

**************

The two main central banks in the advanced capitalist economies, the US Federal Reserve and the European Central Bank (ECB), raised their ‘policy’ interest rates again this week. The policy rate sets the floor for all borrowing rates in these economies. Both central banks hiked their rates by another 0.25%, so the Fed’s rate now stands at 5.25% and the ECB’s at 3.7%. This compares with just 0.25% and 0% respectively two years ago.

The professed aim of these hikes is to ‘control’ inflation and drive the currently high rates back to the so-called target rate that both central banks have of 2%. I and others have argued firmly, with evidence, that this monetary tightening policy will have little effect on getting inflation down because the causes of inflation do not lie in excessive money supply (the monetarist theory) or in excessive wages driving up prices (the Keynesian theory). Neither of these theories is backed up empirically.

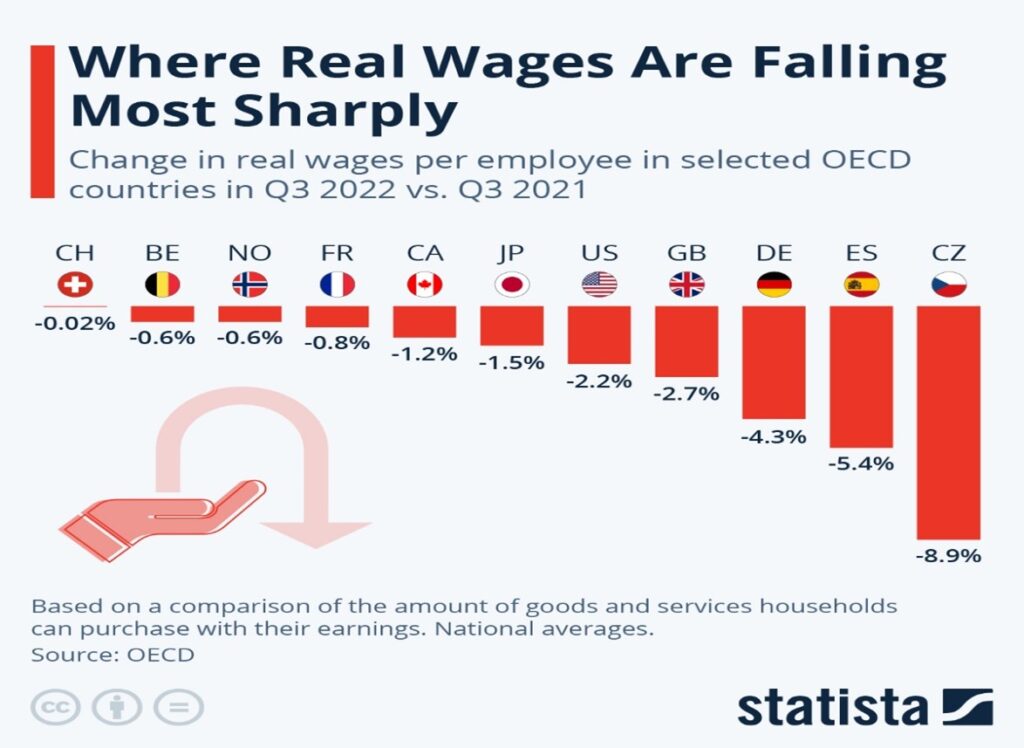

Profits, not wages, have gained from Inflationary spiral

The reason for the accelerating inflation of the last two years is to be found in the restriction of supply, both in production and transportation, partly from supply-chain blockages after the COVID slump, partly from the Russia-Ukraine war and partly from very low productivity growth in the major goods sectors of the world economy. The shortage of supply has enabled the multi-national energy and food producers to raise prices to extremes – see the huge profits made by the oil majors. These raw material costs have then been fed through by corporations in price rises to the ‘end consumer’ – mostly households. It’s been profits that have gained the most from the inflationary spiral, not wages. Real wages (ie after deducting inflation) in just about every economy have fallen in the last two years.

Over the last two years there has been an average rise in prices of around 15% (and much higher in energy and food). The headline inflation rate in the major economies has only just started to subside because of the end of supply-side blockages and because the major economies are slowing fast towards a recession and real incomes are falling. The monetary policies of the Fed and the ECB have not been the drivers of inflation reduction. And yet, the central bank leaders continue to parrot the story that this painful process of interest rate increases cannot be avoided and is the only way to get inflation down. Remember the comments of Bank of England chief economist: Huw Pill: “Somehow in the UK, someone needs to accept that they’re worse off and stop trying to maintain their real spending power by bidding up prices, whether through higher wages or passing energy costs on to customers etc.”

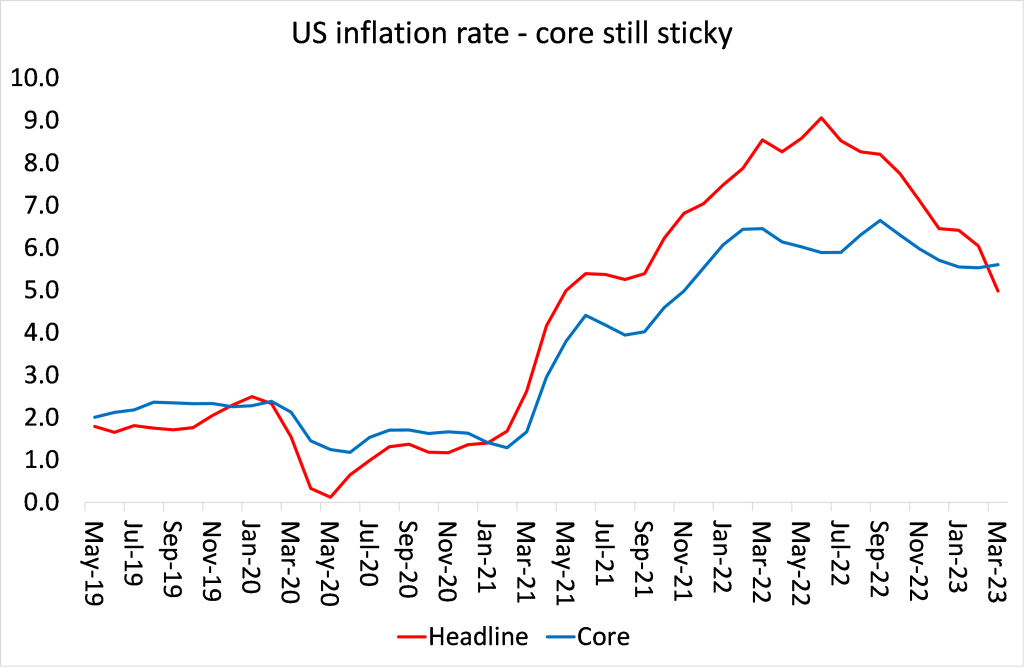

Inflation rates remain ‘sticky’

If you strip out the falling prices of energy and food, the underlying inflation rates in the US and Europe remain ‘sticky’. Indeed, ‘core’ inflation is still close to 6% yoy in both areas, more than three times the central banks’ target of 2% inflation.

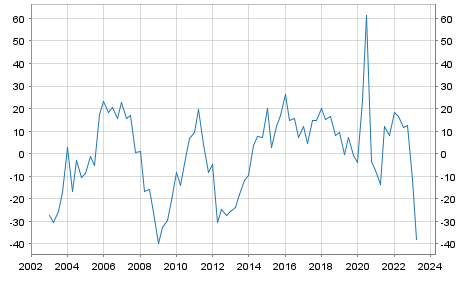

The impact of central bank rate hikes has not been so much on driving down inflation as on accelerating economies into a slump; and on generating a banking crisis as weaker banks collapse in the face of rising borrowing costs and falling prices of the bond assets they hold. In Europe, the big drop in the demand for loans by both households and companies is a telling sign of the impact of monetary tightening – while the liquidation of the historic Swiss bank, Credit Suisse, is an indicator that the banking crisis is not confined to the US.

Eurozone loan demand dives

In the US, it is a similar story. There the banking crisis rolls on, first with the collapse of First Republic Bank last week, swallowed up by JP Morgan with sweeteners from the government; and then immediately after the latest hike by the Fed, the news that another Californian bank PacWest had called for extra finance in order to survive. The small banks stock index has dived as investors fear further busts ahead.

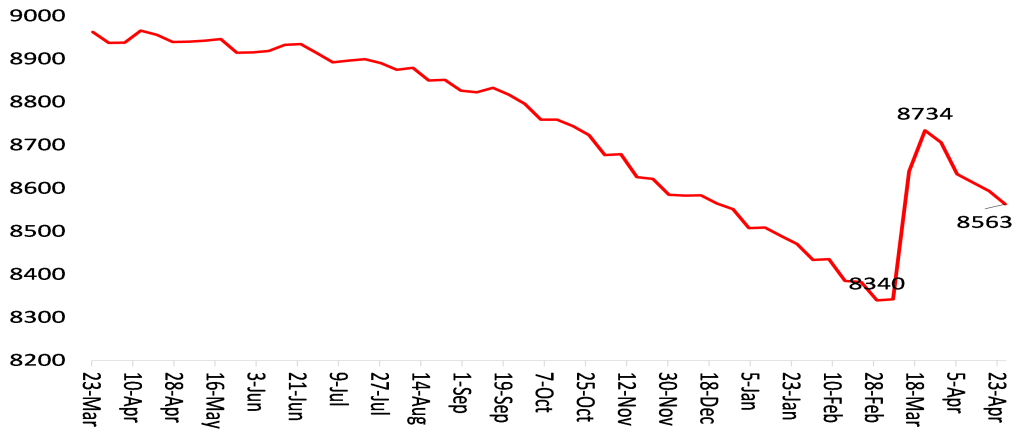

Despite this, Jay Powell, head of the Fed, argues that the banking crisis is under control (like inflation) and that recession in the US economy will also be avoided – even though the Fed’s own economists are forecasting a “mild recession” in the next two quarters of this year, before any recovery. Indeed, despite the banking debacle, the Fed has returned to reducing its bond holdings (ie tightening credit).

Federal Reserve balance sheet $bn

But behind the confident tone of Powell lies uncertainty. The Fed appears likely to hold off further hikes and hope that inflation will fall without any further measures. In the Fed’s press conference, Powell commented: “I mean there is a sense that, you know, we’re much closer to the end of this than to the beginning. That, you know, as I mentioned, if you add up all the tightening that’s going on through various channels, we feel like we’re getting close or maybe even there.” But he also made clear that there was no prospect of any reduction in the policy rate either. So the pain will continue.

The ECB was even more hawkish. ECB President Lagarde said in her press conference that “We are not pausing and have further to go. We are continuing the hiking process. We are on a journey and have not got there yet.” She was explicit that the aim of the ECB was to drive down the economy. “Headline inflation is coming down and credit lending is slowing. But this tighter monetary policy has not affected the ‘real economy’ yet. We need to see that leg of the process happen.”

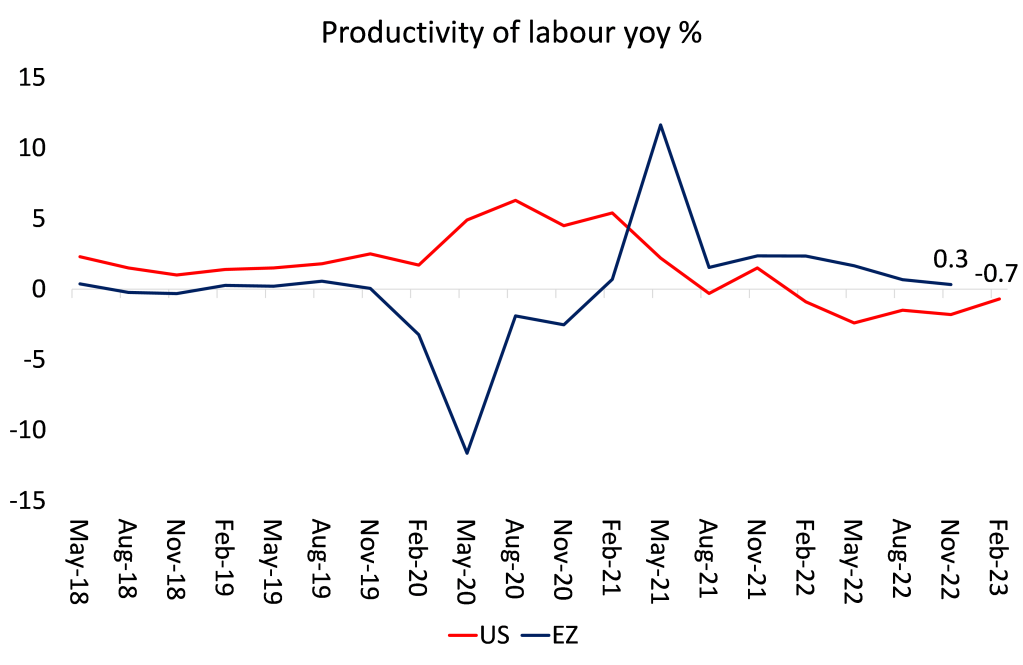

Wages and the productivity of labour

Workers, particularly in Europe, are fighting hard to restore their losses in real incomes by obtaining increased wages. But that can only mean lower profits if there is no increased productivity out of the workforce. And productivity growth is falling in the US, down 2.7% in the first quarter of this year and more or less flat in the Eurozone.

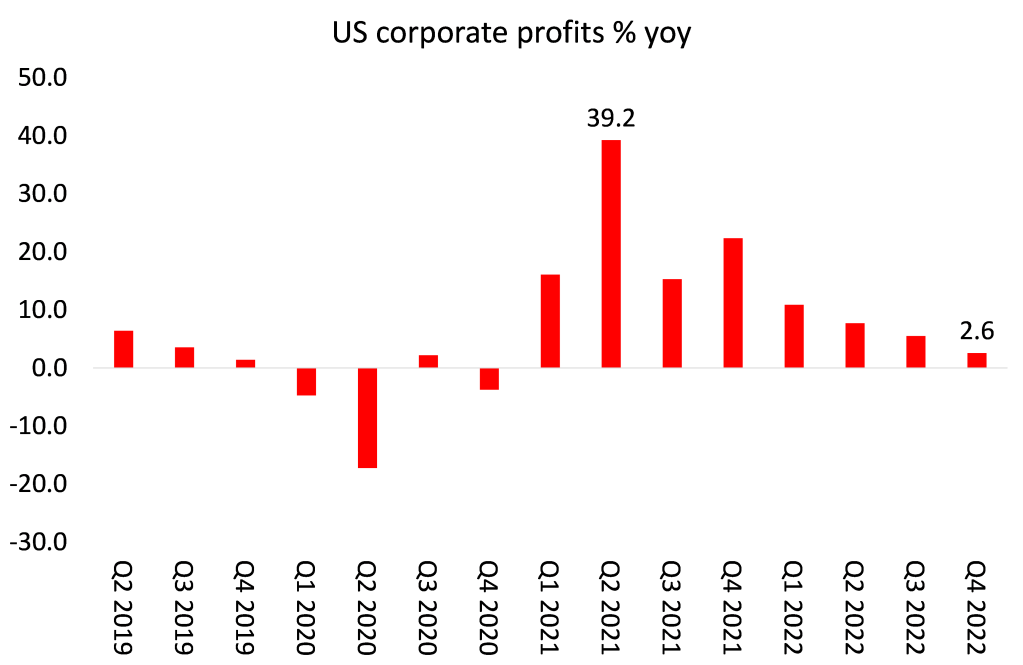

Profit margins (profit per unit of production), having reached historic highs last year, are falling back and total corporate profit growth is slowing fast.

This will lead eventually to falls in productive investment and bankruptcies among the smaller and weaker corporations. Inflation rates will then fall (even though they will still be higher than before COVID), but only at the expense of rising unemployment and recession.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.