By Michael Roberts

At the beginning of this year, I wrote a post on how the capitalist mode of production was in what some call a ‘polycrisis’, where various crises: economic (inflation and slump); environmental (climate and pandemic); and geopolitical (war and international divisions) had come together in the early 21st century. Polycrisis, the new buzzword among leftists, is in many ways similar to my own description of the contradictions of the Long Depression of the 2010s that have to come to a head in the 2020s.

Now, as the main international economic agencies, the IMF and the World Bank, meet in Marrakech this week, it is worth updating what is happening to these strands or contradictions that make up the polycrisis of capitalism.

Record temperatures highlight lack of progress on climate change

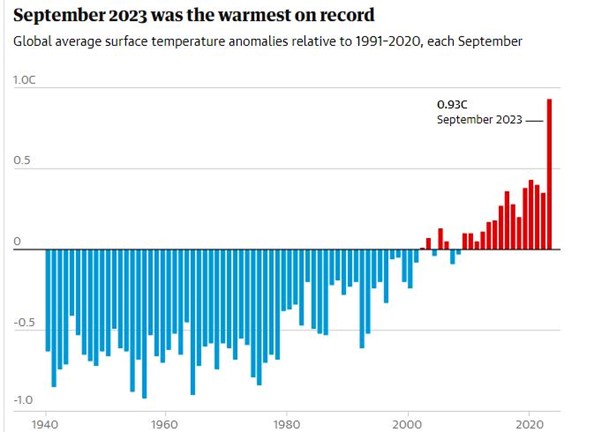

Let’s start with the climate and global warming. Global temperatures soared to a new record in September by a huge margin. Scientists at the Copernicus Climate Change Service said 2023 was on course to be the hottest on record, after the average global temperature in September was 1.75C degrees warmer than the pre-industrial period of 1850-1900, before human-induced climate change began to take effect.

The hottest September on record follows the hottest August and hottest July, with the latter being the hottest month ever recorded. September 2023 beat the previous record for that month by 0.5C, the largest jump in temperature ever seen. This record heat is the result of the continuing high levels of carbon dioxide emissions combined with a rapid flip of the planet’s biggest natural climate phenomenon, El Niño. And this “extreme month” has likely pushed 2023 into the “dubious honour of first place” as the hottest year ever, with temperatures about 1.4C above pre-industrial average temperatures.

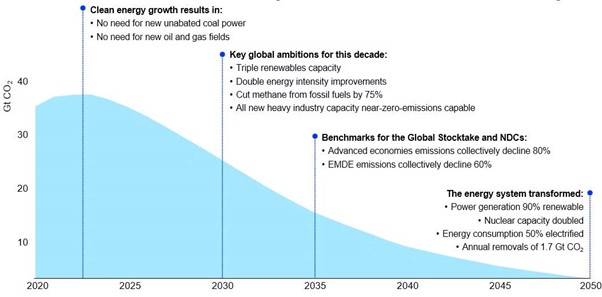

The world is way off track to tackle climate change and remains headed for a temperature rise of up to 2.6C and must take urgent action, said UNCTAD in its latest report on the global economy. UNCTAD said countries needed to be “more ambitious in action” and set “more ambitious targets” in order to cut emissions by the required 43 per cent by 2030 and by 60 per cent by 2035 compared with 2019 levels, in order to avert the dire consequences of a warmer planet. This would require a “radical” transformation of systems across all sectors, including boosting renewable energy, ending the use of all fossil fuels without the emissions captured, cutting methane and other greenhouse gases, ending deforestation and improving energy efficiency.

Government pledges and actions falling well short of what is needed

None of this is happening to any degree necessary. The International Energy Agency (IEA) says fossil fuel demand must fall by more than 25% by 2030 and 80% in 2050. And by 2035, emissions need to decline by 80% in advanced economies and 60% in emerging market and developing economies compared to the 2022 level. But current Nationally Determined Contributions are not in line with countries’ own net zero emissions pledges, and those pledges are not sufficient to put the world on a pathway to net zero emissions by 2050. The “emissions gap” consistent with limiting warming to 1.5C in 2030 was as much as 24bn tonnes higher than it needs to be.

Global finance for climate action reached about $803bn annually for 2019-20, less than a fifth of the estimated $4tn annual investment in clean energy technology needed to limit temperature rises to 2C or 1.5C. Meanwhile global fossil fuel subsidies have hit a record high of $7tn in 2022, the IMF estimates. The IMF study said subsidies for coal, oil and natural gas in 2022 were equivalent to 7.1 per cent of global GDP. This represented more than governments spent on education, and two-thirds of what was spent on healthcare.

At the recent G20 meeting, one of the key policy actions necessary to save the planet; namely the end of fossil fuel production, was ignored. “To have any chance of meeting the Paris Agreement’s 1.5°C temperature limitation goal, sharp reductions in the production and use of all fossil fuels … are essential, and on that issue, the G20 leaders are missing in action,” Alden Meyer, senior associate at E3G, the climate consultancy, said. Behind that failure lies the huge and grotesque profits made by the oil and gas giants in the post-pandemic inflation period. Their ‘reluctance’ to ‘strand’ their stock of assets (ie not use them or explore for more) is no surprise.

‘Carbon credits’ and ‘carbon taxes’ policies don’t work

What policy answers have been offered by companies and governments to end global warming? First, we have the ludicrous ‘carbon offsets’ schemes. Many of the largest companies in the world have used ‘carbon credits’ for their sustainability efforts from the unregulated voluntary market, which grew to $2bn (£1.6bn) in size in 2021 and saw prices for many carbon credits rise above $20 per offset. The credits are often generated on the basis they are contributing to climate change mitigation such as stopping tropical deforestation, tree planting and creating renewable energy projects in developing countries. Investigations show that more than 90% of their rainforest offset credits – among the most commonly used by companies – are likely to be “phantom credits” and do not represent genuine carbon reductions.

Then there are carbon taxes and prices. This market solution to deter the use of fossil fuels is the main plank of the IMF to solve global warmings. Carbon pricing schemes just hide the reality that, as long as the fossil fuel industry and the other big multinational emitters of greenhouse gases are untouched and not brought into a plan for phasing them out, the tipping point for irreversible global warming will be passed. Instead of waiting for the market to speak, and for ‘regulation’, we need a global plan where fossil fuel industries, financial institutions and major emitting sectors are brought under public ownership and control.

There are two months to go until countries meet in Dubai at the UN COP28 climate summit. Given that this international climate conference is being hosted by a leading oil and gas producer, don’t expect any radical action on fossil fuels.

Billions living in poverty worldwide

Then there is poverty and inequality. At this week’s meeting, the World Bank will present a new report on poverty. According to the World Bank, global poverty has now receded to levels closer to those prior to the pandemic, but this still means that we have lost three years in the fight against poverty. The recovery is also uneven: while extreme poverty in middle-income countries has decreased, poverty in the poorest countries and countries affected by fragility, conflict or violence is still worse than before the pandemic.

After much criticism of its ludicrously low threshold for poverty globally, the Bank now offers three levels. In 2023, 691 million people (or 8.6% of the global population) are projected to live in ‘extreme poverty’ (i.e., those living below $2.15/day), which is just below the level prior to the start of the pandemic. At the $3.65/day line, the poverty rate and the number of poor are both lower than in 2019. At the more realistic (but still very low) $6.85/day level, a smaller share of the global population also now lives below that compared to before the pandemic. But due to population growth, the total number of poor living below this line is still higher than before the pandemic. And when we look at the poorest countries, they still have higher poverty rates than before and are not ‘closing the gap’.

These poverty rates are misleading, as I have shown here. Nearly all the recorded reduction in global poverty (whatever the level used) in the last 30 years is due to China taking around 900m Chinese above those levels. Exclude China and global poverty has hardly fallen either in share or numbers. Indeed, even including China, there are still 3.65bn people on the planet below the $6.85/day poverty line, according to the World Bank.

In 2021, Lloyd’s Register Foundation partnered with Gallup and polled 125,000 people from 121 countries, asking how long people could cover their basic needs without income. The study found that a staggering 2.7 billion people could only cover their basic needs for a month or less without income, and of that number, 946 million could survive for a week at most. The UN target to end ‘poverty’ by 2030 is a mirage.

Global hunger affecting the health of children around the world

Global hunger is still far above pre-pandemic levels. It is estimated that between 690 and 783 million people in the world faced hunger in 2022. This is 122 million more people than before the COVID-19 pandemic. It is projected that almost 600 million people will be chronically undernourished in 2030. So the UN target of zero hunger by then is way off track. More than 3.1 billion people in the world – or 42 percent – were unable to afford a healthy diet. Worldwide in 2022, an estimated 148.1 million children under five years of age (22.3 percent) were stunted, 45 million (6.8 percent) were wasted, and 37 million (5.6 percent) were overweight.

Of a total of 2.4 billion people in the world facing ‘food insecurity’ in 2022, nearly half (1.1 billion) were in Asia; 37 percent (868 million) were in Africa; 10.5 percent (248 million) lived in Latin America and the Caribbean; and around 4 percent (90 million) were in Northern America and Europe. One billion Indians cannot afford to eat a healthy diet. That’s 74% of the population. India does slightly better than Pakistan, but is behind Sri Lanka. The corresponding number for China is 11%.

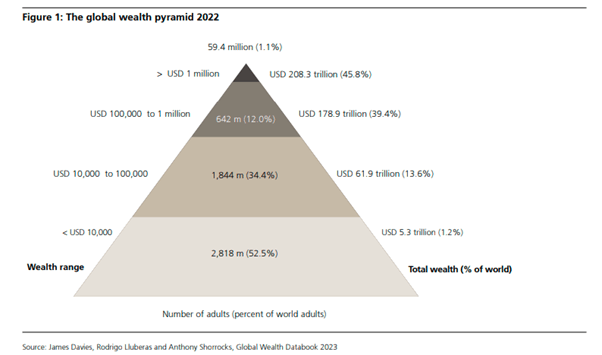

World wealth pyramid shows huge disparity in personal wealth

And then there is inequality of wealth and incomes. The latest Credit Suisse report on global personal wealth showed that show that in 2022, 1% of adults (59m) owned 44.5% of all personal wealth in the world, slightly higher than before the pandemic in 2019. At the other end of the wealth pyramid, the bottom 52.5% of the world’ population (2.8bn) had net wealth of just 1.2%.

As for wealth inequality within countries, the Gini coefficient (the usual measure of inequality) for wealth was a huge 85.0 in the United States (remember 100 would mean one adult owning all the wealth). Indeed, in the United States, all measures of inequality have trended upward since the early 2000s. For instance, the wealth share of the top 1% of adults rose from 32.9% in 2000 to 35.1% in 2021 in the United States.

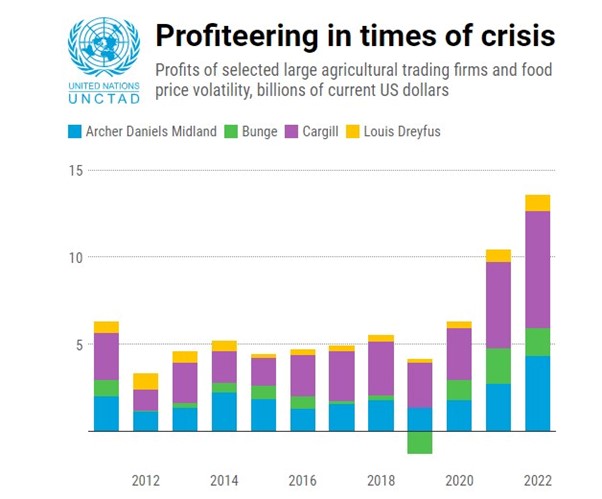

Huge rise in food costs: large agricultural trading companies cash in

UNCTAD reports that “During the period of heightened price volatility since 2020, certain major food trading companies have earned record profits in the financial markets, even as food prices have soared globally and millions of people faced a cost-of-living crisis.”

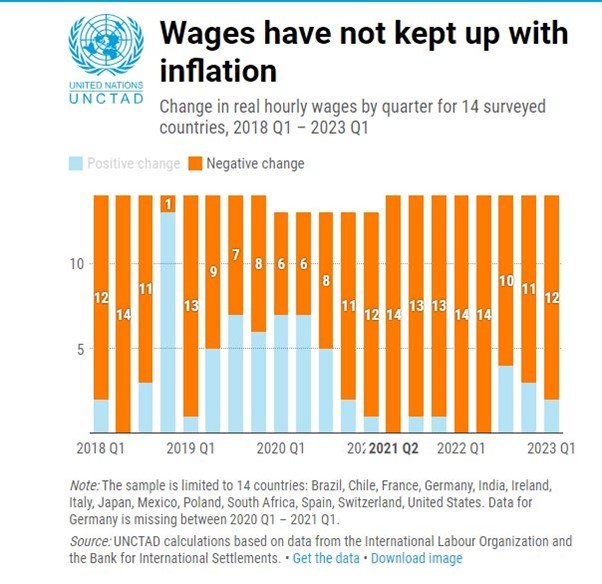

Indeed, the pandemic and the subsequent inflation surge have left their mark on the incomes of the average household. Take the UK: never in living memory have working families got so poor, according to the think-tank, the Resolution Foundation. “This parliamentary term is on track to be by far the worst for living standards since the 1950s. Typical working age household incomes are on course to be 4% lower in 2024-25 than they were in 2019-20. Never in living memory have families got so much poorer over a parliament.”

Nobel (Riksbank) prize winner in economics (2015), Angus Deaton has a new book out called ‘Economics in America: an immigrant economist explores the land of inequality’. In it, he attacks the failure of neoclassical economics to address in any way the issues of poverty and inequality. Mainstream economists in the US deliberately ignore rising levels of inequality and the horrendous impact of poverty, claiming that this is not the business of economics. And yet “real wages have stagnated since 1980 while productivity has more than doubled and the rich cream off the profits. The top 10% of US families now own 76% of wealth. The bottom 50% own just 1%.” A class system now operates and “the war on poverty has become a war on the poor”.

Deaton points out that more equality will not be achieved simply by tax transfers and welfare payments – they will hardly make a dent. The answer for him is state spending and investment in education and jobs for all. Deaton opposed more radical policies: “We do not need to abolish capitalism or selectively nationalize the means of production. But we do need to put the power of competition back in the service of the middle and working classes. There are terrible risks ahead if we continue to run an economy that is organized to let a minority prey on the majority.” But is not a tiny minority preying on the majority the very essence of class societies and modern capitalism? In my view, Deaton’s policy solution is just as utopian as taxation, as it does not address the control and ownership by capital of the means of production and employment of labour that ensures that a tiny minority have the vast bulk of wealth and income while society as a whole does not have enough to meet even basic needs.

Global debt rises to a new high

The pandemic and subsequent rise in inflation and interest rates globally has exposed many of the poorest countries in the world to debt default. They owe billions to creditors, both public and private, in the so-called Global North. This they can only pay back by cutting services and any spending to meet the needs of their citizens – and increasingly they are unable to pay at all.

Global debt has hit a new high according to the International Institute of Finance (IIF). Total debt — spanning sovereigns, corporates and households — rose by $10tn to about $307tn in the six months to June, or 336% of world GDP. The World Bank estimates that 60 per cent of low-income countries are heavily indebted and at high risk of debt distress, while many middle-income countries also face significant budgetary challenges.

Central bank hikes have therefore also sharply driven up the costs of borrowing, which from the IMF can currently be up to 8 per cent. The burden of paying high interest rates to the IMF is worsening. “If the IMF’s worst-case scenario of deteriorating global economic conditions materialises, demand for IMF support will surge even more.” So an IMF debt trap! The IMF at this week’s meeting will warn that governments “should take urgent steps to help reduce debt vulnerabilities and reverse long-term debt trends”. But how? There are no proposals by the rich countries to write off these debts; or end the trade tariff and constraints on emerging market exports; or of course, stop the huge extraction of profits from the resource-rich, poor countries by multi-national companies.

Economic crisis connects all the strands of the ‘Polycrisis’

Global warming; unending global poverty and inequality; debt disaster: all these strands in the ‘polycrisis’ of capitalism in the 21st century are connected through the burgeoning economic crisis.

Global trade is falling at its fastest since the pandemic. Trade volumes were down 3.2 per cent in July compared with the same month last year, the steepest drop since the early months of the coronavirus pandemic in August 2020, according to the CPB. The about-turn in export volumes is broad based, with most of the world reporting falling trade volumes. China, the world’s largest goods exporter, posted a 1.5 per cent annual fall, the Eurozone a 2.5 per cent contraction, and the US a 0.6 per cent decrease. The CPB also reported that global industrial production fell 0.1 per cent compared with the previous month, driven by sharp falls in output in Japan, the eurozone and the UK – and is also down year on year.

The World Bank has just issued a report prior to this week’s meeting in which it reckons that Asia faces one of worst economic outlooks in half a century. The previously called ‘Asian tigers’ of Korea, Taiwan, Singapore, Hong Kong etc are set to expand at one of the lowest rates in five decades, as US protectionism and rising levels of debt pose an economic drag. The World Bank forecast that China’s growth would slow to 4.4 per cent in 2024, the lowest rate in decades, although still more than double the rate of any G7 economy. The worsening forecasts also reflect that much of the region is starting to be hit by new US industrial and trade policies under the Inflation Reduction Act and the Chips and Science Act.

Prospects for the world economy

The latest UNCTAD report on the world economy reckons that the world economy has stalled and the risks over the coming year are rising. UNCTAD forecasts that “stuttering growth for the period 2022-24 will fall short of the pre-Covid rate in most regions of the world economy. Debt burdens are crushing too many developing countries. Debt service on external public debt relative to government revenues surged from nearly 6% to 16% between 2010 and 2021.”

There is much optimism in the US that the economy will achieve a ‘soft landing’ i.e the inflation rate will soon fall back to the target rate of 2% a year without real GDP contracting into a recession. I have discussed the likelihood of that in a previous post. Even if that turns out to be the case, a ‘soft landing’ does not apply to the rest of the major advanced capitalist economies. The Eurozone area is contracting; as are Canada, the UK and several smaller economies like Sweden, while Japan is on the cusp.

Indeed, the Organisation for Economic Co-operation and Development (OECD), in its latest report, forecasts global growth in 2024 will be lower than in 2023 falling from 3% this year to 2.7% in 2024. Despite the global economy proving “more resilient than expected” in the first six months of 2023, the growth outlook “remains weak”. Real GDP growth in the advanced capitalist economies will slow from 1.5% this year to just 1.2% in 2024 and GDP per capita will be close to contraction.

The OECD economists reckon inflation will not return to pre-pandemic levels any time soon, so central banks must keep interest rates high. Indeed, the IMF also calls for central banks to keep up the misery of debt burdens in the ‘war against inflation’. Yet, as I have argued, because higher inflation was a ‘supply-side’ problem, central bank money tightening does little to reduce inflation and is only a recipe for ‘slumpflation’.

Weakening of US dominance in world affairs

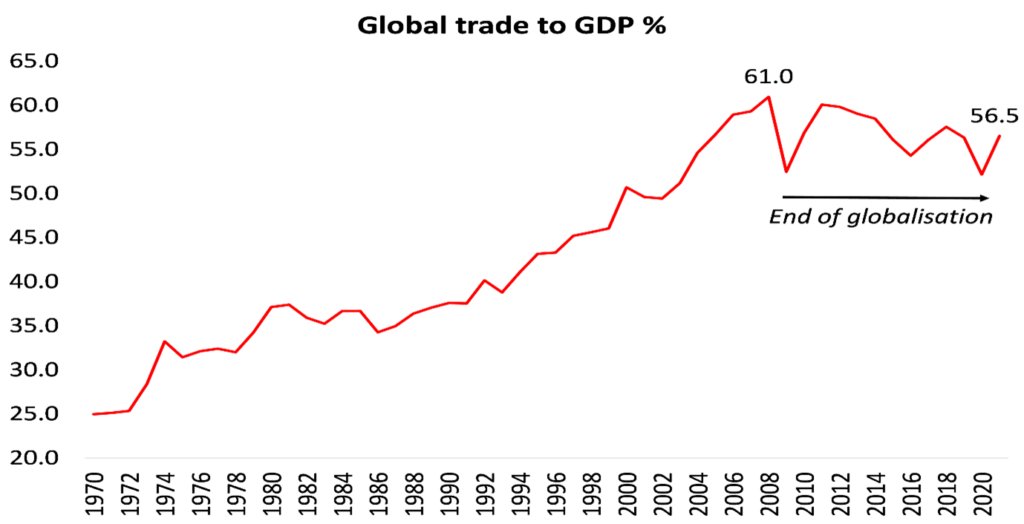

And there are two other strands in the polycrisis of the 21st century that still have to unfold. There is the weakening of US dominance in world affairs. ‘Globalisation’ of trade and finance over the last 40 years under the hegemony of the US is over.

US capital’s ability to expand the productive resources and to sustain profitability has been declining. This explains its intensified effort to strangle and contain China’s rising economic strength and so maintain its hegemony in the world economic order. A recent study by Sergio Camera showed “a prolonged stagnation” of the US rate of profit in the 21st century. The general rate of profit was 19.3% in the ‘golden age’ of US supremacy in the 1950s and 1960s; but then fell to an average 15.4% in the 1970s; the neoliberal recovery (coinciding with a new globalisation wave), pushed that rate back up to 16.2% in the 1990s. But in the two decades of this century the average rate dropped to just 14.3% – an historic low.

That has led to lower investment and productivity growth in the decade of what I have called the Long Depression of the 2010s, so that, to use Sergio’s words, the US “economic base has been seriously debilitated”. This is weakening the hegemonic position of US capitalism in the world. Now there is what is described as ‘geopolitical fragmentation’ ie the rise of alternative blocs attempting to break with the imperialist bloc led by the US. The Russian invasion of Ukraine highlights this ‘fragmentation’.

What the world needs is global cooperation to overcome the polycrisis of capitalism. Instead, capitalism is fragmenting as it is inherently incapable of international unity and global planning. The economic costs of this fragmentation have been measured: in trade of up to 7% of world GDP; with the addition of technological decoupling, the loss in output could reach 8-12% in some countries.

The additional disruptive factor of Artificial Intelligence

Longer term is the growing disruption to economies of the rise of AI. Goldman Sachs economists reckon that if the new AI technology lived up to its promise (which is in doubt), it would bring “significant disruption” to the labour market, exposing the equivalent of 300m full-time workers across the major economies to automation of their jobs. They calculate that roughly two-thirds of jobs in the US and Europe are exposed to some degree of AI automation, based on data on the tasks typically performed in thousands of occupations.

Humanity and the planet are facing an existential crisis from global warming and climate change; but will human labour be replaced by thinking machines even before the climate catastrophe, thus widening inequalities and increasing wealth for the machine owners (capital) and poverty for the billions (labour)? The polycrisis of capitalism in the 21st century has only just begun.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.