By Michael Roberts

Last weekend, I delivered a keynote lecture to economics students at Britain’s Open University on their Economics Day. The venue was at the London School of Economics, but the LSE was not involved in organising the meeting. This is a transcript of my presentation.

Today I have been asked to speak on the topic of: Why ‘real world economics’ matters? That title begs a few questions: What is real world economics? And this implies that there is economics that is not about the real world. And if there is real world economics, what can it contribute to making a better world for us all?

What real world economics should be about

Real world economics should be about understanding what is happening in the world around us: what causes inflation, unemployment, poverty, inequality, climate change etc. And what are the economic policy answers. But there is a problem. What I call mainstream economics does not discuss or deal with these real world issues very well.

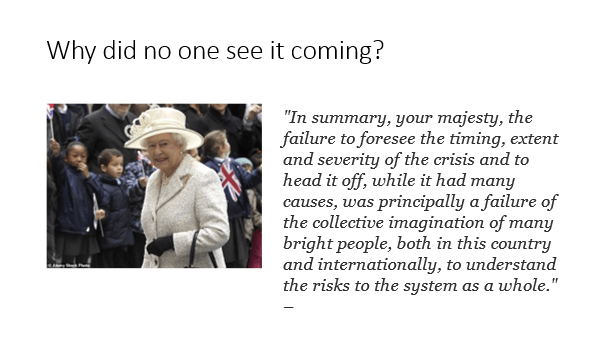

One example directly involving this very building springs to mind. Back in the depth of what came to be called the Great Recession of 2008-9 when all the major economies were suffering a sharp and deep fall in national output, employment and average incomes, after a humungous collapse in the banking and financial systems, Queen Elizabeth visited the London School of Economics.

As she stepped into this very building, she asked the gathering of eminent economists who met her: “Why did no one see it coming?” In other words, she asked why no one had predicted the financial collapse and the ensuing slump, the worst since the 1930s depression years. The eminent economists were nonplussed by the Queen’s question about the real world. It took them three months before they responded – in a published three-page letter to the Queen.

I quote: “Everyone seemed to be doing their own job properly on its own merit. And according to standard measures of success, they were often doing it well. The failure was to see how collectively this added up to a series of interconnected imbalances over which no single authority had jurisdiction.” I think the economists were saying that their theories seemed to be fine but then lots of different things that they knew about somehow all came together in a perfect storm to create the crash and they could not have foreseen that.

Six months later the Queen visited the Bank of England and one of the Bank’s top financial policy experts stopped the Queen to say he would like to answer the question she first posed to those economists at the LSE. He told the Queen that financial crises were a bit like earthquakes and flu pandemics in being rare and difficult to predict and reassured her that the staff at the Bank were there to help prevent another one. Prince Philip did not miss his opportunity: “so is there another one coming?” No answer.

Mainstream economists thought that depressions were no more

But here is my point. It’s not just that the economists didn’t notice it coming ‘out of the blue’ like an asteroid hitting the earth, a shock to a perfectly working economic system. Their theories assumed away the possibility entirely.

Robert Lucas is an eminent mainstream economist, indeed a Nobel prize winner for economics. In 2003, some five years before the global financial crash he pronounced that “macroeconomics has succeeded: Its central problem of depression prevention has been solved, for all practical purposes, and has in fact been solved for many decades.”

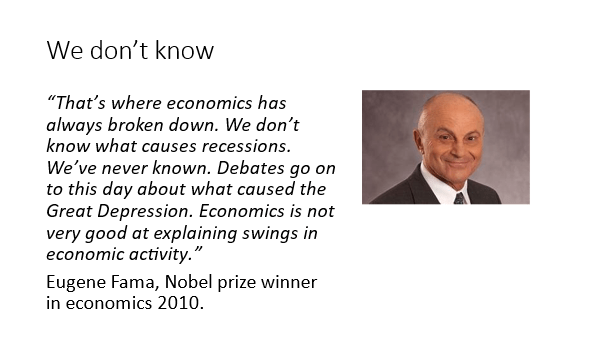

Eugene Fama is another Nobel prize winner in economics. His prize is for showing that markets work efficiently and, as long as you and me and everybody has enough information about what is going on, then the market will ensure full employment, steady growth and rising incomes for all. This is called the Efficient Markets Hypothesis (EMH). After the Great Recession, Fama was asked what went wrong. He replied, “We don’t know what causes recessions. We’ve never known. Debates go on to this day about what caused the Great Depression. Economics is not very good at explaining swings in economic activity”.

Up to now I have talked about one economics event and one strand of explanation: what I have called mainstream economics and its failure to forecast or deal with that event, i.e. global financial collapse of banks and a deep contraction in employment and incomes globally. A real problem but with no answer from the mainstream. But that poses the question that if mainstream market economics cannot explain the real world very well, then we need new theories to guide our policy decisions.

The mainstream is divided between the neoclassical and the Keynesian schools

And there are other theories. Indeed, we can categorise economics into various schools, with the main division between ‘mainstream’ and ‘heterodox’. In the mainstream, we have two great sub-divisions. The first is called the neoclassical school. This school starts from a basic assumption that a ‘free market’ ie. without interference or imperfections caused by monopolies or trade unions or the government, will deliver harmonious economic improvement in what is called a ‘general equilibrium’. As one neoclassical economist once put it: ‘the market economy is like a calm lake or pool. Sometimes a rock or stone can disturb it, a shock to the calm environment, but eventually if those interferences stop, the ripples in the pool will subside and the pool will be calm again’.

Within the mainstream, there is also the Keynesian school, named after the theories of John Maynard Keynes, the great British 20th century economist. Keynesian theory rejects the equilibrium idea of the calm pool of the neoclassical school. The Keynesians think the neoclassical model is not ‘real world’ economics. The Keynesians argue that market economies sometimes get into ‘disequilibrium’ leading to depressions and unemployment, which economies do not get out of unless governments intervene with measures including printing more money or increasing government spending to restore equilibrium.

But both the neoclassical and Keynesian schools agree on one thing: that a market-based system is the only viable form of economy. It’s just that one school thinks that ‘harmonious’ growth can be achieved by a free market without interference and the other thinks government and central banks must intervene to correct any disequilibrium.

Both mainstream schools are based on the primacy of the market economy

But mainstream economics starts from an assumption that it has not proved – namely that a market economy where companies employ people like us to produce goods and services to sell on a market for money – and more importantly for profits for the owners and shareholders of those companies – is the only way to organize the production and distribution of things that we humans need.

But the market economy has not always existed – indeed it has been around for only about 250 years. Before that there were feudal economies where peasants or serfs worked the land for their masters who consumed the produce. That system was around for over 1,000 years. Before that there were slave economies where people captured in wars were forced to work for their slave owners – that system was around for thousands of years.

I make this point because we should be aware that how economies are run now has not always been here and may not last as the best way to meet the needs of humanity. Indeed, in my view, the market economy shows significant signs of failing to do so. So there may be other ways of economic organization.

The heterodox economists criticise the mainstream

As such, there are economists who have serious criticisms of mainstream market economics. There is what we can call the heterodox schools of economics – the term meaning what it says, outside the orthodox mainstream. Within this broad strand, these economists highlight the irrational behaviour of markets and the inherent instability of the market economy. They include the Marxist school which argues the market economy will always have crises that cannot be resolved by the market and so the market economy (called capitalism by Marxists) needs to be replaced by a planned economy based on common ownership of all producers.

The heterodox school is very critical of the mainstream. Indeed, almost exactly six years ago, leading heterodox economists held a seminar right here at the LSE on the state of mainstream economics, as taught in the universities. They kicked this off by nailing a poster with 33 theses critiquing mainstream economics to the door of this building. (You can google it). It was the 500th anniversary of when Martin Luther nailed his 95 theses to the Castle Church, Wittenberg which provoked the beginning of the Protestant reformation against the ‘one true religion’ of Catholicism.

The heterodox economists were telling us that mainstream economics was like Catholicism and must be protested against as Luther did back in 1517. As they put it, “Economics is broken. From climate change to inequality, mainstream (neoclassical) economics has not provided the solutions to the problems we face and yet it is still dominant in government, academia and other economic institutions. It is time for a new economics.”

The alternative models proposed by the heterodox economists

What should that new economics be? Recently, Benoît Cœuré, a leading French member of the Executive Board of the European Central Bank, delivered an address just like I am doing now to you, to economics students at the Paris School of Economics, if you like, the sister university to the LSE. Cœuré told his student audience that “economics is a social science. Models will not take away the burden and responsibility of making judgements. Economics involves much trial and error – you have to take decisions in the fog when you can barely see your hand in front of your face. This makes our profession exciting!”

For me, economics is a science – if a social science dealing with humans, not a physical science. As a science, it requires scientific method. For me, that means you start with a hypothesis that has realistic assumptions that have been ‘abstracted’ from reality and then construct a model or set of laws that can be tested against evidence. The model can use mathematics to refine its precision, but eventually the evidence decides. In my view, like physicists and astronomers, economists too must be able to develop theories about the economies in the real world and test them empirically so that we can make predictions and hopefully avoid the economic crises that modern economies have on a regular basis.

Up to now, I have discussed the big events like the Great Recession and the contribution or failure of mainstream economics to forecast or explain them or provide effective economic policies to remedy them and avoid more in the future. But much of mainstream economics is not about these big events. Benoit Cœuré in his Paris lecture dismissed the criticism that economists failed to predict the outbreak of the financial crisis. “This criticism is nonsense. Do we expect physicians to predict illnesses? We don’t, of course. But we expect them to help us cure illnesses. Economists should do the same.” So it’s not the job of economics to forecast or predict but to develop policies to cure any messes that emerge.

The idea that economists should just fixing things after the event

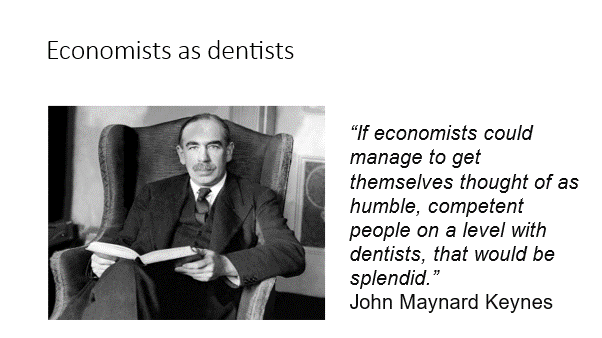

This is a common theme among economists. Another recent Nobel prize winner, Esther Duflo, reckoned economists should give up on the big ideas and instead just solve problems like plumbers “lay the pipes and fix the leaks”. Economists were more like engineers than physicists. Keynes made a similar point: that economists should be like dentists – sorting out troublesome teething problems so that capitalism can then run smoothly.

Duflo reckons the analogy of plumbers means that pure scientific method of analysing cause and effect was less important than practical fixes. So economists should be more like doctors than medical researchers. Plumbers, dentists, engineers, doctors – but not, it seems, social scientists.

The lessons from health care disprove this analogy

But are doctors all that matter in human health? Actually, improved doctoral skills in treating patients once they have become ill comes from scientific discovery about diseases, biology and the environment. Successful drugs and medical practices are the result of learning what the cause of the illness is.

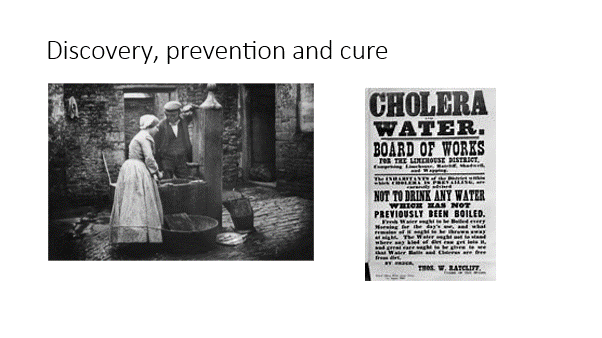

In medieval times, doctors applied all sorts of useless and dangerous treatments (leeches etc) because they did not know about ‘germs’ (bacteria or viruses). Cholera was eventually abated by a geographical study in London showing it was prevalent near bad drinking wells. Malaria and smallpox were resolved by discovering the carriers of the bacteria in various animals. Treatments by doctors then followed.

Of course, that does not mean economics is not about understanding an economy at micro or small levels and coming up with policies to change things for the better – the right taxes to raise funds for government programmes and achieve better equality; suitable price caps to curb energy prices; the right congestion charges to reduce fossil fuel traffic, clear cost benefit analysis to gauge whether the HS2 rail should be built or not. This is also part of economics.

Indeed, this is the sort of economics and policy making that most economists do and probably how you would make a living if and when you graduate and stay in economics. And you could do well. Couere explained to his Paris students that becoming an economist was a great thing to do and paid well. “For many, a master’s degree is a natural step towards a PhD. And a PhD is essentially a promise of employment. In the United States, for example, the unemployment rate for PhD economists is about 0.8%, the lowest among all sciences. Not a bad place to start from.” But said Couere, the money was less important because “your PhD should be fuelled by your passion and your love for research rather than by hopes of earning more money.”

I am sure that is the case for all of you too. However, I must be blunt here. Cœuré’s experience in the public sector may be different from those of us who have worked in the private sector. Having worked in the private sector, in banks and other financial institutions in my ‘career’, economic policy advice and making things better for all is not the target, but instead it is ‘how to make money’. Economics there is geared to either corporate strategy for profits in production and trade or to investment strategy for profits in financial speculation.

Real world economics must look at the ‘big picture’

In my view, real world economics must look at the ‘big picture’. Economists should not be just doctors but social scientists, or more accurately they should develop an economics that recognises the wider social forces that drive economic models. That is called political economy, mostly not taught in universities. Let me remind you of some of the big picture economic issues that will affect us all much more than anything like whether the HS2 rail line is built or income taxes should be raised or reduced.

First, there is global warming and climate change. The international Cop28 is meeting in Dubai right now on how to reduce greenhouse gas emissions – what is needed is a 43% reduction in emissions by the end of this decade if the world is to avoid an average increase in global temperature more than 2C above pre-industrial levels.

What are the economic theories and policies that can achieve that reduction? It is worrying to know as the LSE’s own Nicholas Stern, the world’s leading climate economist, has noted: “Economics has contributed disturbingly little to discussions about climate change. As one example, the most prestigious mainstream Quarterly Journal of Economics, currently the most-cited journal in the field of economics, has never published an article on climate change!”

Then there is the issue of global poverty and rising inequality of wealth and income between nations around the world and within nations. According to the World Bank, there are around 3.65bn people living on less than $6.85 a day. There are over 700m people facing daily hunger. There are over 3bn people not eating a healthy diet and so getting ill, obese, or even wasted. Is it morally right or even good economics that the top 1% of the world’s adults own nearly 50% of all the personal wealth in the world while the bottom 50% have only 1%? What can we do about this?

Mainstream economics ignores income inequality

Angus Deaton is a British Nobel prize winner in economics and an expert on poverty economics, working in America. In a recent book, Deaton angrily said that “mainstream economists deliberately ignore rising levels of inequality and the horrendous impact of poverty, claiming that this is not the business of economics. …. “there is this very strong libertarian belief that inequality is not a proper area of study for economists. Even if you were to worry about inequality, it would be best if you just kept quiet and lived with it.”

Then there is the technology of the 21st century: robots, automation, artificial intelligence, in particular the emergence of super-intelligent language learning models (LLMs). Have you used LLMs like ChatGPT yet for leisure – but hopefully not for writing automatic dissertations for your professors? Apparently, four out of five British teenagers are using it for school work, according to Ofcom, the technology regulator. What does all this mean for your future jobs when you graduate – will AI have replaced you before you graduate? Some economists estimate that 300m jobs will go globally. Here is another vital area for real world economics.

I finish by saying to you all: remember that there is a world out there beyond supply and demand curves and mathematical formulae.

Economics and economists should not be sucked into just being like dentists fixing teeth, but also use their skills and the scientific method to understand the big picture and so help to make a better world for all. Then perhaps we can avoid being visited by King Charles at some time in future and have him repeat what Queen Elizabeth said: “why did you not see that coming?”

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.