By Michael Roberts

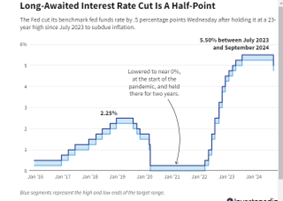

Last Wednesday’s decision of the US Federal Reserve Bank’s monetary committee to cut its ‘policy interest rate’ is significant in two ways. First, it signals that the Fed reckons that the ‘war against inflation’ is over. The Fed’s cut was the first since 2020. The last few years since the end of pandemic slump have seen a very sharp rise in the policy rate from nearly zero in 2021 to 5.5% in 2023.

The policy rate acts a floor for all rates of borrowing by households for mortgages and consumer credit and for companies for loans and bond prices in the US. But not just in the US. The world’s corporations and governments borrow money mainly in dollars. So the Fed’s policy rate affects indirectly borrowing rates in all countries, particularly those with heavy debt obligations in the Global South. The Fed’ s high interest rate has driven up the debt servicing burden for the poorest countries, many of which are in ‘debt distress’, some even defaulting on their payments.

This cut in the base rate is relatively high

Second, the Fed cut is significant because of the size of the reduction. The Fed committee decided to reduce the policy rate by 50bp (0.5%), not 25bps as is usual. This implies two things: one rosy and one not so rosy. It suggests that the Fed is confident that the US inflation rate will continue to drop down towards the 2% a year policy target. The Fed measures inflation using the change in prices for personal consumption expenditure (PCE) and the PCE rate is now down to 2.3% and the Fed projection is that this rate will fall to the target of 2% by 2026 (so still some two years away).

But it also suggests that the US economy is showing significant signs of slowing down. Real GDP growth has averaged around 2.2% in the first half of 2024. But that growth rate is forecast to slow in the third quarter just ending. The St Louis Federal Reserve forecast is for 1.6% in this current quarter, although the Atlanta Fed forecast is higher at 2.9%. The US manufacturing sector remains in a slump despite the construction boom in AI infrastructure. The unemployment rate has been edging up to levels that some indicators would suggest a coming recession.

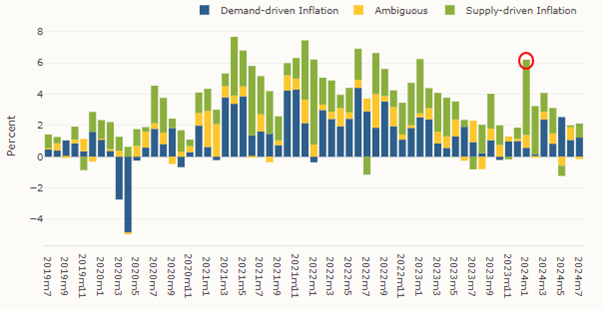

The Fed’s PCE measure of inflation underestimates real inflation

In addition, using the PCE inflation seriously underestimates inflation. The main reason for the rise in inflation since 2022 has been the rise in energy and food prices driven by the disruptions in international supply chains after the pandemic and poor productivity growth ie supply factor. It was not due to ‘excessive’ government spending or ‘excessive’ wage rises ie demand factors. The evidence for this from many studies is overwhelming.

The fall in the ‘headline’ inflation rate has been mainly due to a decline in the rise of energy and food prices. Underneath that, ‘core’ price inflation has not declined by nearly so much. Core PCE inflation is still around 2.6% a year in the US. And if various components of household spending (insurance, mortgages etc) were properly included in the inflation basket, it would tell a different story, putting the inflation rate several points higher than the PCE measure. The Fed’s monetary policy actions did not stop inflation rising and had little to do with it subsequently falling.

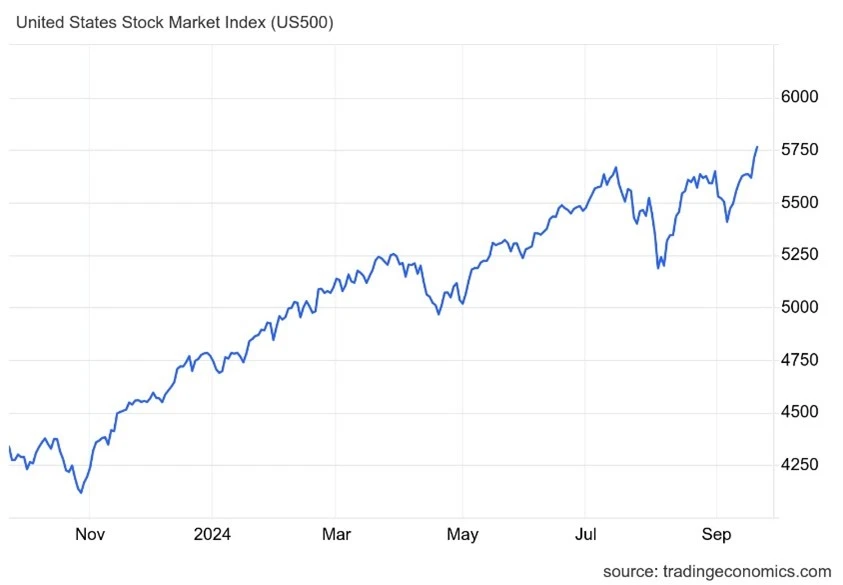

Stock and bond markets react to the cut in the rate

Nevertheless, the Fed claims that inflation has been subdued by the Fed’s monetary policy and most important, without causing a slump in the economy. The Fed committee’s projections are for 2% a year real GDP growth, 2% inflation and an unemployment rate stabilising at about 4.4% – in other words, a perfect ‘soft landing’ for the economy; a ‘Goldilocks scenario’ of an economy neither ‘too hot’ nor ‘too cold’, but just right. This scenario is echoed by all the major mainstream economists in the major investment banks and so is swallowed by the majority of financial investors. As a result, the US stock and bond markets hit new highs after the Fed rate cut.

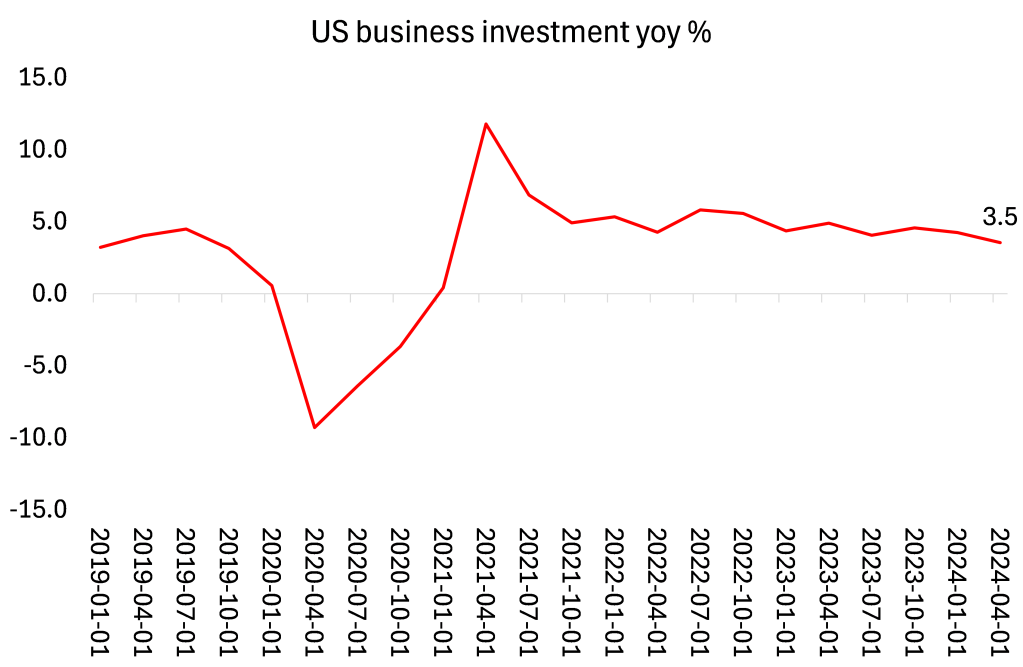

I’ve discussed the nature and likelihood of this so-called ‘soft landing’ in a previous post. Suffice it to say at this point, I don’t think that the US economy is going into a recession just yet. Corporate profits are holding up and giving financial support to some investment, although most of these profits are being made by the mega-tech Magnificent Seven companies and most of the investment is by these companies in AI and chip infrastructure, partly subsidised by the Biden administration.

The vast swathe of the US corporate sector is struggling, particularly small businesses, hit by high interest rates, poor demand for their goods and services and increased costs of inputs and services.

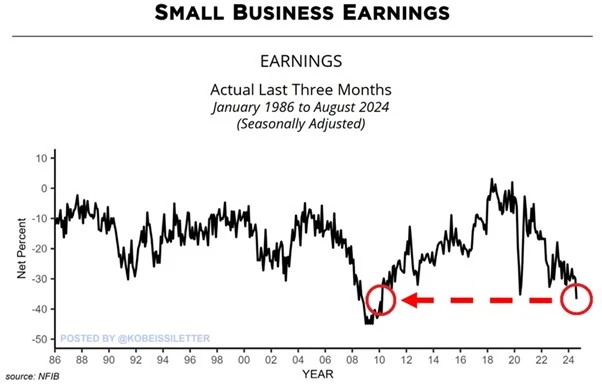

Small businesses really struggling

Around 37% of US small businesses have seen their earnings drop over the last 3 months, the highest share in 14 years. This is even weaker than the 35% seen during the 2020 pandemic. Small businesses are struggling as if the economy is in a recession.

Poor growth forecast for the rest of the decade

Also there has to be a sense of proportion here. Financial investors may be excited by the start of a series of reductions in interest rates making it it cheaper to borrow and speculate in ‘fictitious capital’, but the US ‘real economy is hardly motoring. The Fed forecasts just 2% a year in real GDP for the rest of this decade. That rate is well below the average growth rate before the Great Recession of 2008-9 and before the pandemic, but that means a much lower rate of real GDP per person as the population expands through immigration.

And the US economy is the best performing of the top seven major capitalist economies (G7). Germany is in a slump, the UK, France and Italy are flatlining; Canada and Japan are stagnant. Only the smaller southern European economies in Europe are doing better and they are coming from a very low base. As for the so-called ‘emerging economies’ of the Global South, South Africa is in a slump; Brazil is crawling; Russia is only growing as a ‘war economy’, while China and India’s fast-growing economies are also showing signs of slowing down. The Fed rate cuts will do nothing to change these trends.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.