By Michael Roberts

Every year the Historical Materialism journal holds a conference in London. It is attended by (mostly) academics and students (mostly of a Marxist viewpoint) to discuss Marxist theory and the issues of the day. The theme this year was: Countering the plague: the forces of reaction and war and how to fight them.

This year was heavily attended with over 930 registered to discuss 800 papers submitted over four days. Also, there was a lecture from last year’s winner of the annual Isaac Deutscher prize for the best book of 2023 (Heide Gerstenberger’s Market and Violence) and there were some very large plenaries on 21st century imperialism and Climate and Capital (see pix below).

I cannot possibly cover all the subjects discussed over four days, so in this review, as usual, I shall concentrate on the sessions on Marxian economics (HM covers all aspects of the Marxist view of human society: philosophy, culture, political strategy etc).

Speakers on the relevance of ‘Late Capitalism’ by Ernest Mandel

Let me start by recounting the sessions that I participated in. The first was a round table discussion of the impact and relevance today of Late Capitalism, a book written by the Belgian Marxist Ernest Mandel in the early 1970s. In my view, this was a landmark work on the nature of and trends in world capitalism in the mid-20th century. This session was called over a new edition of the book with an introduction by Cedric Durand, the French economist. There were several well-known speakers: Peter Green, Ozlem Onaran, Riccardo Bellofiore, Alan Freeman and myself.

Peter Green gave Mandel’s book some pluses and minuses; one plus was that Mandel criticised the ‘monocausal’ view of crises ie that there is one main cause of crises, rather a multiplicity. One minus was Mandel’s lack of support for a disproportion theory of crises. Peter was also not convinced by Mandel’s support for long waves in capitalist accumulation (ie upwards for decades and then downwards).

Ozlem Onaran, who ironically is (was) a member of the particular Trotskyist group of the 20th century associated with Mandel (the Mandelists) reckoned that Late Capitalism now needed to be expanded in its scope to cover feminism, unpaid care and to find a way of ‘synthesizing’ Marxist economic theory with post-Keynesian Kalecki theory! I doubt that if Mandel had been at this session he would have agreed.

Riccardo Bellofiore went further and basically dismissed most of Mandel’s approach on crises and in particular his attachment for Marx’s law of the tendency for the rate of profit to fall. Alan Freeman concentrated his remarks on Mandel’s indefatigable revolutionary work.

‘Late capitalism’ and the question of ‘monocausality’

I found myself pretty much in disagreement with the other speakers. For me, Mandel made great strides in explaining the long boom after WW2; and showing that ‘late capitalism’ was just that, still capitalism. It had not morphed into ‘monopoly capitalism’, or ‘state monopoly capitalism’, or ‘financialised capitalism’, where profitability was no longer the touchstone of capital accumulation. Mandel continued to base himself on Marx’s law of profitability to explain crises.

However, I reckoned that Mandel had weakened the strength of this theory by criticising what he called ‘monocausal’ explanations of capitalist crises, in particular Luxemburg’s underconsumption theory and Grossman’s mass of profit theory. Mandel claimed instead that there were multiple causes: the falling rate of profit was the basis of the crisis in production; but there was also a ‘realisation’ crisis caused by a lack of demand from ‘final consumers’.

I took the opportunity, somewhat tongue in cheek, to raise the banner of ‘monocausality’, namely that if we accept a multiplicity of causes and those causes are different for each crisis in capitalist production, then we have no theory of crises at all. In my view, it is clear that behind crises in capitalism is the profit motive and Marx’s law of profitability is the underlying (but not proximate) cause of crises. From a fall in profitability and the mass of profit comes a collapse of investment and eventually output, income, employment and consumption – not vice versa. See here for a better explanation of what I mean.

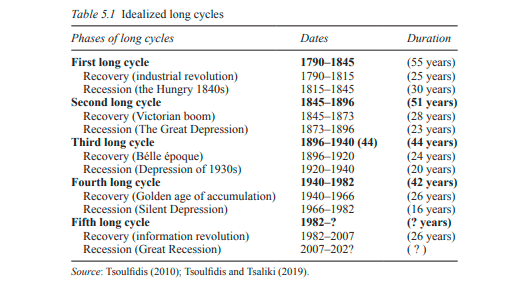

The long waves theory of capitalism accumulation

Another key part of Mandel’s analysis of capitalist accumulation was his version of the long waves theory of capitalist accumulation, namely that accumulation has a period of relatively successful expansion with new technologies, but then a downward wave of relative decline driven by falling profitability and the exhaustion of existing technologies. It think the empirical evidence for long waves or cycles is increasingly well supported and relevant to giving us a ‘long view’ on the state of the world economy (see my book, The Long Depression and there are other new works that I shall review soon). Long waves indicate the objective situation from which we can draw some political strategy (the subjective).

However, Mandel in Late Capitalism attempts to reconcile this ‘endogenous’ theory of economic cycles first presented by Kondratiev with Trotsky’s view that political factors must instead drive cycles. So he ends up with a mish mash in his explanation. For me, the upward swing of accumulation relates to a period of rising profitability and the downward phase relates to when the rate of profit falls. Economic crises create the conditions for a new rise in profitability based on new technologies that bring about a new upward wave.

This approach is accused of being ‘mechanistic’ and again at the session, I raised the banner of being a mechanist. Since Mandel wrote Late Capitalism, a pile of new empirical work has been produced that supports endogenously caused long waves.

Since Mandel wrote Late Capitalism, global manufacturing has mainly moved out of the imperialist advanced capitalist economies to the periphery; the Soviet Union has collapsed and China has emerged as a major economic rival to US hegemony. Neoliberal policies have destroyed the ‘welfare state’ of the immediate post-war period and ended confidence in Keynesian macro management policies to end booms and slumps. Instead there have been sharply rising inequalities in incomes and wealth, both between and within countries. Above all, climate change from global warming, driven by profit-seeking ‘fossil capitalism’, has become a major existential challenge to humanity and nature. It’s time for a new book on ‘later capitalism’ in the 21st century.

Session on the causes of inflation

I’ve taken up a fair bit of space in this post on one session, so let me move on to the session on the causes of inflation and policies to deal with it that I also participated in. In this session, Bill Dunn from Kingston University in the UK presented a counter-intuitive argument on the politics of inflation in arguing that price inflation is not always bad for working people. Bill reminded us that when you have a lot of debt, you can inflate some of the debt burden away. And in the aggregate, inflation could be conducive to faster economic growth. Indeed, when workers’ demands for higher wages are met by objections that they induce inflation, labour could argue that inflation is not the terrible evil that it is painted.

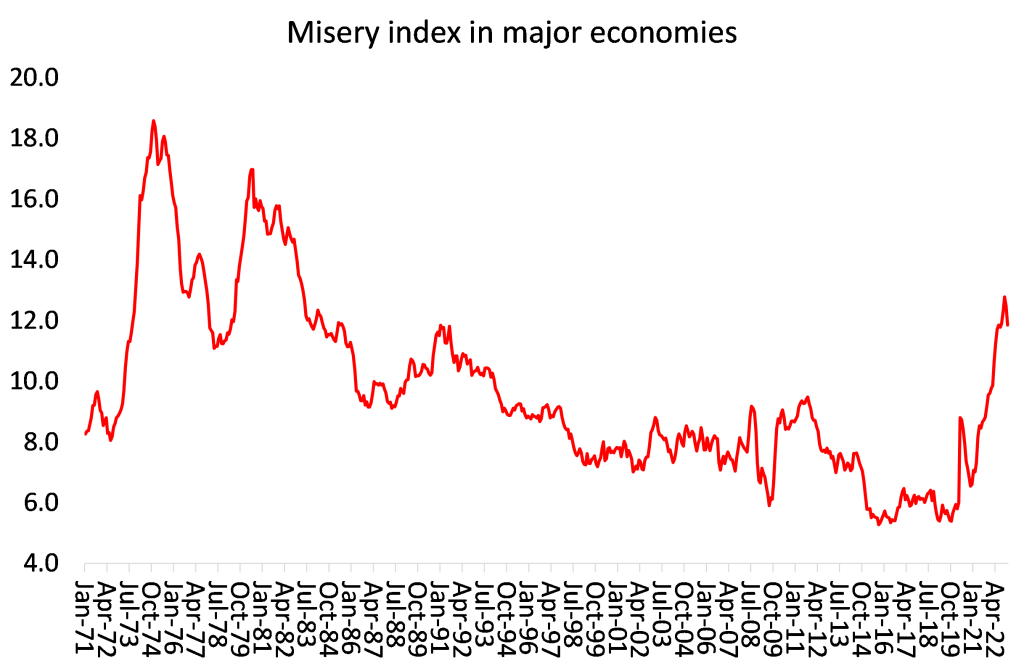

I must say that I did not consider Bill’s arguments for a less anti-inflation view by the left very convincing. I am pretty clear that the recent post-pandemic inflation spike in all the major economies seriously damaged the real incomes of most working-class households. As a result, it was a key factor in Trump’s sweeping victory in the US presidential election just before HM started.

Take the global ‘Misery Index’ (an index of the unemployment rate plus the inflation rate). The impact of high inflation in 2021-2 drove up the misery index to levels globally not seen since the 1970s.

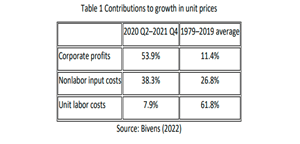

In my view, it is capital, not labour, that likes a bit of inflation (not too much, mind) as providing room for capitalists to hike prices to sustain profits. Indeed, in my presentation, I showed evidence for a profit-price spiral in the recent post pandemic inflation.

A value theory of inflation

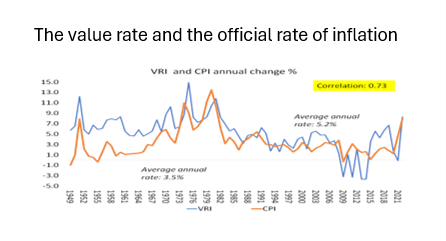

My presentation was based on joint work with Guglielmo Carchedi on the underlying causes of inflation. We argue that the mainstream monetarist, Keynesian cost push and the psychological ‘expectations’ theories are false. Instead, we offer a value theory of inflation. This argues that, as in Marxist theory aggregate values equal prices of production and money is a representation of that value, so ceteris paribus, if value grows, money supply will rise to match that value growth and so there will be no inflation in prices. However, new value growth (which we measure in hours of labour worked by the whole labour force in an economy) tends to slow relative to increased output of commodities. So prices per unit of output should tend to fall as less labour time is involved in the production of output.

But that does not happen. Why not? Because the monetary authorities in capitalist governments are tied to a monetarist theory that claims that if they boost money supply that will restore any slowdown in the growth of value. That leads to a gap between the growth in (circulating) money and new value growth. The difference between the two is the ‘value rate of inflation’. Using US data, we find that over the post-war period that the value rate has tended to fall. In the first sub-period up to the 1980s, the gap widened, so the value rate rose (inflation and stagflation); but in the second period after the 1980s to now, the gap narrowed and the value rate slowed (disinflation and deflation). We found a very good positive correlation between our value rate of inflation and the official inflation (in the US), empirically supporting our theory of inflation in modern economies.

What can you conclude from this? First, our value rate of inflation is consistently higher than the official rate. That tells you that the official estimate of inflation significantly underestimates the true rate of inflation in modern economies. Second, it tells you that if the monetary authorities boost the money supply when value growth is slowing, there will be price inflation (unless the extra money does not circulate, but goes into buying financial assets or is hoarded in bank accounts, as happened in the 2010s with so-called quantitative easing).

The determinate factor in the movement of prices

Interestingly, our theory has affinities with Mandel’s ‘permanent inflation’ theory as expounded in Late Capitalism, where he says that if “money circulation has doubled without a significant increase in the total labour time spent in the economy, then the price level will tend to double too.” And the quantity of money is “always combined with given ups and downs of the rate of profit, of the productivity of labour, of output, of market conditions (overproduction or insufficient production)”. But in our theory, we have defined much more clearly the determinate factor (value growth) and the determined or counteracting factor (money supply) in the movement of prices. As a result, Carchedi and I reckon the value theory of inflation has a better explanatory power over the mainstream theories and also offers some predictive power on the direction of future inflation.

So much for the sessions I participated in. In my second post on the year’s HM conference I shall discuss what I learnt in other sessions that I attended.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.