By Michael Roberts

COP26 trundles on in Glasgow with little sign that anything significant is being agreed towards reversing global warming and ending the degradation of nature. Beneath all the media headlines, governments and corporations are not putting their money where their mouths are. The financial support for measures to reduce carbon emissions and other destruction of the environment is pitiful.

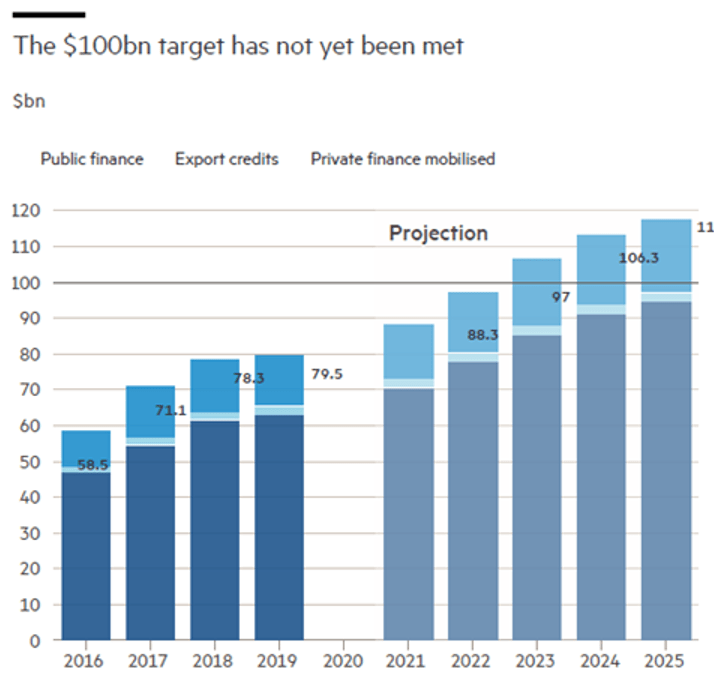

In 2009, the major rich nations promised they would send at least $100bn a year in climate finance to poorer countries by 2020. That understanding formed the basis of the 2015 Paris climate accord, which aimed to limit global warming to well below 2C, ideally 1.5C. But on the eve of COP26, donor countries admitted they had missed that target in 2020. Now they expect to reach it in 2022 or 2023, years later than planned.

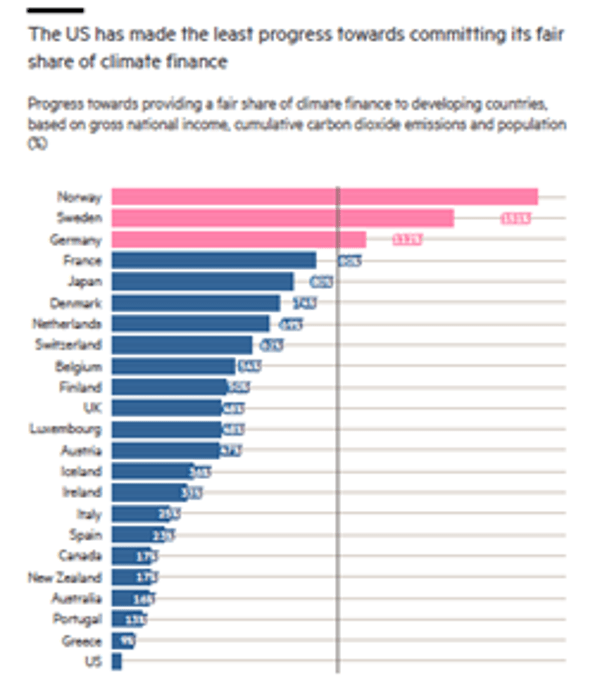

Indeed, most of the rich nations are not meeting their promises at all. Only Norway, Sweden and Germany can claim that, while the US is billions short and at the bottom of the OECD list.

Moreover, most of the pledged $100bn is not in the form of grants but loans. So poor countries trying to deal with global warming and to reduce emissions are supposed to pay the bulk of the rich countries’ handouts back. Calculations from Oxfam suggest the true level of climate-specific grants is about one-fifth of the OECD “climate finance” numbers, once loans are taken out.

Bloomberg and Carney joint chairs

These climate commitments were “a mile wide and an inch deep”, Becky Jarvis, a strategist for the Bank on our Future campaign network, said.

Then there is the Mark Carney-led coalition of international financial companies signed up to tackle climate change. Former Bank of England governor Carney is the official UN envoy on climate finance. He claims that the Glasgow Financial Alliance for Net Zero (Gfanz) — which is made up of more than 450 banks, insurers and asset managers across 45 countries — could deliver as much as $100-130tn of financing to help economies transition to net zero over the next three decades.

Michael Bloomberg, the media billionaire, was joining Carney as co-chair. The group will report on its work periodically to the G20’s Financial Stability Board. Carney pointed to UN analysis that suggested the private sector could deliver 70 per cent of total investments needed to meet net zero goals. Private finance can save the day – argues Carney.

But when you look more closely at this headline figure, you find that investment managers account for $57tn of the assets, with $63tn coming from banks and $10tn from asset owners such as pension funds. And 43 of these 221 investment manager signatories revealed that only one-third of their assets were aimed at investments with ‘net-zero’ targets.

Not a fresh pool of money and most cannot be allocated

Ben Caldecott, director of the Oxford Sustainable Finance Group at Oxford university, said the headline $130tn figure was “not a fresh pool of money, and most of it isn’t allocatable”. It included home mortgages and money to fund fossil fuel infrastructure, he added. “What proportion of it can you actually divert into the solutions or use in a way to influence polluting companies to become more sustainable?” he asked.

The Rainforest Action Network, an environmental group, pointed out that the 93 banks that had signed the pledge continued to provide $575bn of lending and underwriting to the fossil fuel industry in 2020. “The disconnect between climate commitments and boardroom decisions is staggering,” said Tom Picken, its forest and finance director.

Asset managers that had signed up to Gfanz had so far aligned just 35 per cent of their total assets to net zero targets, she said. “It is not green finance, nor is it all dedicated in the slightest to tackling climate change as long as financiers have large interests in fossil fuel expansion,” she added. “This announcement yet again ignores the biggest elephant in the room,” said Richard Brooks, Stand.earth climate finance director. “There is no mention of the F words at all in this new declaration from the net zero clubs. We cannot keep under 1.5 degrees [warming] if financial institutions don’t stop funding coal, oil and gas companies.”

Funding problems within the market economy

Meanwhile, well-meaning economists offer various schemes to solve the funding problem within the confines of the market economy. Raghuram Rajan, professor of finance at the University of Chicago’s Booth School of Business, renowned from his pro-market solutions, suggests that every country that emits more than the global average of around five tonnes per capita pay annually into a global fund.

The amount paid would be the excess emissions per capita multiplied by the population and further multiplied by a dollar amount called the GlobalCarbon Incentive (GCI). If the GCI started at $10 per tonne, the US would pay around$33bn each year. Meanwhile, countries below the global average would receive a commensurate payout based on how much they emit below the average (Uganda,for example, would receive around $2bn).

Rajaram sees the scheme as self-financing. Low emitters, often the poorest countries and the ones most vulnerable to climatic changes they did not cause, would receive a payment that could help their people adapt. Conversely, the responsibility for payments would appropriately lie with big rich emitters, who are also in the best position to pay.

Countries would be free to choose their own domestic path to emissions reduction. Instead of levying a politically unpopular carbon tax, a country might impose regulations on coal, another might incentivise renewables.

“We need a settlement on an aspiration”

In another scheme, Avinash Persaud points out that to meet the Paris agreement, the world would have to eliminate 53.5 billion metric tonnes of carbon dioxide each year for the next 30 years. There are a range of estimates of how much that would cost, but the investment bank Morgan Stanley put it at an additional $50 trillion, split between five key areas of zero-carbon technology. That compares with pathetic $100 billion mentioned above that has taken six years for countries to scrounge together. Persaud says “we need a global settlement – not global aspiration attached to a village hall budget.”

The countries that contribute most to the stock of GHGs could issue an instrument that gives any investor in projects anywhere in the world that reduce GHGs the right to borrow from them at their overnight interest rates – which are currently near zero – and to roll over this borrowing for as long as the project delivers some minimum rate of reduction in GHGs per dollar invested. If the collective annual issuance of this near-zero cost funding were $500 billion, it would boost investor returns to such a degree that it would over 15 years crowd in private savings to the $50trillion needed.

All these schemes fail on two levels. First, they require global action and global institutions to implement them. There is no prospect of that happening. Just as national governments failed to coordinate finance and resources to deal with the COVID pandemic and vaccinations, so governments are unwilling to take significant global action on climate and nature.

Around $50trn over 30 years is needed apparently – other estimates are $4trn a year for the next ten years. This is really a small cost, no more than 2.5% of annual world GDP. But so far governments have pledged just $100bn and have not even met that.

Private finance organised by banks will not deliver

Second, market solutions will not do the trick, as again the COVID pandemic has shown. Only government intervention, investment and planning on a global scale can give humanity and nature a chance to succeed before too much degradation is made permanent. Carbon pricing will not allocate investment properly or change consumption sufficiently – and it only benefits the richer countries (1bn people) at the expense of the poorer (6.5bn).

Private finance organised by banks and investment funds will not deliver. That’s because capitalist companies control and make decisions on investment based on profitability. Global warming will not be stopped or reversed without ending fossil fuel and mining exploration and phasing out fossil fuel production. Nothing like that is on the agenda of COP26.

As Jeff Sparrow says in his new book, Crimes against Nature, “Each year, the world spends over $1,917bn on guns, bombs, and other military equipment. The comparable figure on advertising is some $325bn. Those staggering numbers represent a mere fraction of what we could direct immediately to environmental programs on land, sea, and air. We could begin systemic decarbonisation, closing down coal-fired power stations, and replacing fossil fuels with electricity from renewables such as solar, using the process to reduce rather than increase our energy needs. We could massively expand low-carbon public transport, so that efficient, easy-to-use and convenient electric trains and trams replaced internal combustion engines. We could replan our cities and towns for human convenience rather than for the use of automobiles; we could establish methods of recycling and re-use that genuinely reduced material throughputs.”

From the blog of Michael Roberts. The original, with all hyperlinks, can be found here.