By Michael Roberts

Like Marxist or mainstream economics, Keynesian economics has several strands. There is Keynesian economics seen within the parameters of general equilibrium economics, where changes in income and expenditure, consumption and investment, interest rates and employment will tend to an equilibrium between employment and inflation, as long as there are no exogenous ‘shocks’ to the market economy. If wages and interest rates fall enough, then full employment and investment growth will be achieved.

This is what Joan Robinson, a follower of Keynes, called ‘bastardised Keynesianism’. It removed all the radical features of Keynesian economics, which, to Robinson, politically a quasi-Maoist, were that full employment could not be automatically achieved in modern ‘market’ economies. More likely there would be an equilibrium of underemployment; and that this would be due to uncertainty about the future for capitalists in making investment decisions and irrationality among economic ‘agents’ like consumers and capitalists.

This radical view of Keynesian economics has come to be called post-Keynesianism (PK), with the main proponents being contemporaries of Keynes like Robinson and Michal Kalecki, the Marxian-Keynesian; and later Hyman Minsky, the socialist-Keynesian. Now there is a whole school of post-Keynesian economics, with journals, conferences and think-tanks.

Post-Keynesianism influence on the left

PK economics dominates and influences the views and policies of the left-wing in the labour movements of the major economies (Corbynomics, Sanders etc) – it is the radical wing of Keynesian economics in general, which in turn has dominated the labour movement since Keynes (except for periods since the 1980s when neo-liberal mainstream ‘free market’ theories influenced labour leaders for some decades).

On my blog I have spent much ink explaining where Marxist economics differs from Keynesian economics in all its strands. For me, a Marxist approach to theory and policy better explains the nature of capitalism and what are the right policies for the labour movement to adopt in its struggle against capital and for a better society for all. Indeed, I think that Keynesian economics is a diversion from achieving that, mainly because its analysis of capitalism is wrong. Moreover, its policy conclusion is that capitalism can be fixed or managed to work for all with a few clever policy adjustments.

PK theory, because it appears much more radical (in that it reckons capitalism cannot be easily managed to benefit all) and because many of its exponents would consider themselves socialists (even Marxists), is in these ways even more misleading as it relies on a radical view of Keynesianism, and yet Keynes was hardly the radical that PK followers think he was.

The basic ideas of post-Keynesian economics

So let me once again, examine the basic ideas of post-Keynesian economics.

To do this, I shall draw on a recent post called “The Post-Keynesian World View in Five Principles”, based on a talk that an ‘Alex’ gave to the Berggruen Institute on zoom.

Alex first tells us about the rising popularity of ‘post-Keynesianism’ after the global financial crash and the COVID slump. Alex reckons it has become popular because “financial markets love it, because it does a good job explaining how the economy runs, which is helpful if your paycheck depends on understanding the economy.”

I’m not sure that because financial analysts apparently ‘love it’ that this a good reason to agree with PK. But Alex goes on to explain that PK “gives good causal heuristics for understanding the impact of financial flows on production, and on the economy at large. It also counsels realism about the impact of government policy on economic outcomes. Public debt and private debt are different, the money supply doesn’t cause inflation, private debt does eventually have to roll over and will have real impacts if it doesn’t.”

So, according to Alex, PK tells us better about how the modern economy works and why debt (particularly private debt) matters. One strand of PK, Modern Monetary Theory, has recently enlightened us all on the workings of money in capitalism, Alex reckons, and as he says “MMT originally grew out of the post-keynesian research agenda, and much of its underlying economic model is still very post-keynesian in structure.” My critique of MMT thus also applies to PK.

What drives production in capitalism?

Alex now makes an interesting statement. “In a capitalist economy, production is undertaken for profit and not for use. As such, value is usually measured using the social convention of accounting. Production happens in anticipation of flows of money, just the same as investment and consumption. On this view, things are worth their book value, more or less, and economic actors act based on these book values. What the post-keynesians think is that this represents a good starting point for economic theorizing, to use the quantities that the actors themselves use.”

What does this mean? Alex seems to adopt the basic point of Marx’s law of value: namely that capitalist production is for profit not social use. And we should measure value in money terms as capitalists do. This sounds promising. But then Alex moves straight on to talk about flows of money and investment and consumption. There is no further mention of the role of profit, after having told us that capitalist production is for profit, not investment or consumption. In my view, this is typical of PK followers. They very quickly dispense with profit in their theoretical explanations, as we shall see below.

Profit replaced with a balance sheet view

Having dispensed with the role of profit, Alex tells us that we should instead consider modern economies from a “balance sheet-based view of the economy as a whole. Individual actors have assets and liabilities, incomes and expenditures. Someone’s asset is someone else’s liability, and vice versa. Everything is interrelated through the use of these conventions.”

Thus we move from the underlying driver of capitalist economies: profit and what is happening to profits and profitability to “studying the flow of payments and the accumulation of assets, not the allocation of scarce resources to their most efficient ends. One of the main benefits this approach has is that it rules out some impossible outcomes: not everyone can run a trade surplus, if there’s a trade deficit, either the private sector or the public sector has to run a deficit to finance it.”

So we are rapidly reduced to macro-identities in analysing economies ie Income = Expenditure; public and private sector deficits and surpluses; trade balances etc. But not profit or the origins of profit.

‘Expected Demand’ in the post-Keynesian view

“Our next principle is that everything is expectation.” Alex tells us a key principle of PK is to look at ‘expectations’. “Expectations inform actions, and these actions in turn create reality. Maybe the simplest model of the Keynesian causal cycle is to say that expected demand drives investment, investment drives employment, employment drives wages, wages drive consumption, consumption drives demand, and demand validates investment. Expected demand drives investment, because businesses only invest in added capacity or hiring more workers when they think that more people will want to buy their product in the future than do at the present moment. If they expected the same demand, or less, there would be no need to invest at all. They could keep running the same equipment.”

So here we have it. Investment under capitalism is not driven by profit or profitability after all, but by ‘expectations’, and not even by future profit, but by ‘expected demand’. This drives investment which in turn leads to employment and wages.

But is this the causal sequence in capitalist production and accumulation? In many previous posts, I have highlighted the key macro equation in post Keynesian identities. Here it is again.

National Income = National Expenditure

National Income = Profits + Wages

National Expenditure = Investment + Consumption

So Profits + Wages = Investment + Consumption

If we assume workers spend all their wages on consumption and capitalists invest all their profits, we get:

Profits = Investment

Investment drives Profits in PK theory

According to PK theory, it is Investment that drives Profits, not vice versa. And ‘Expected Demand’ drives Investment (says Alex) and Investment drives Wages and Profits.

Or as Michel Kalecki, whose equation this is, said: ‘workers spend (Consumption) what they get (Wages); and capitalists get (Profits) what they spend (Investment)’.

In my view, this is manifestly a wrong view about the capitalist economy. Instead of Investment driving Profits as above, the reality is that Profits drive Investment. Thus, capitalist investment is not result of the level of ‘expected demand’, or some entirely subjective psychological view of investors having what Keynes called ‘animal spirits’, but the result of an objective measure of previous (and likely profitability) of investment. But as with Keynes, PK does not want to put profits up front, but reduce it to a consequence of investment (or, in reality, to hide it from analysis altogether). For further on this, read the excellent chapter 3 by Jose Tapia in World in Crisis.

“Whackiness in financial markets”

Alex refers to the work of Hyman Minsky, a PK theorist who relied heavily on ‘expectations’ to explain investment decisions. “Hyman Minsky talks about this extensively: if you think an asset’s price is going to skyrocket, you start buying it to make a profit. You can even borrow money against it and use that money to buy more. As the price goes up, the amount you can borrow against goes up as well, and the price starts flying. The whole Gamestop episode last month was a version of this that used call options rather than margin loans, but the principle is similar. The problem comes for Minsky when the borrowing gets cut off: there’s nothing to support the prices and everything crashes down. Sometimes the operation of extreme expectations can create wackiness in financial markets that can have dire consequences for the economy at large.”

So according to Alex (and Minsky) ‘extreme expectations’ create a “wackiness in financial markets” that brings the whole economy crashing down as in the global financial crash of 2008. But why does the whole thing crash after going so well – apparently because of ‘extreme expectations’? But this is an answer that only poses the question of why are expectations fine at one moment and then ‘extreme’ at another. What makes them extreme?

No doubt Minskyites will quote Minsky’s famous phrase that “stability breeds instability’. But again, this is just a clever phrase to cover the fact that PK theory does not have a theory of financial crises except that they happen when things get ‘extreme’.

Marxist economic theory explains recessions

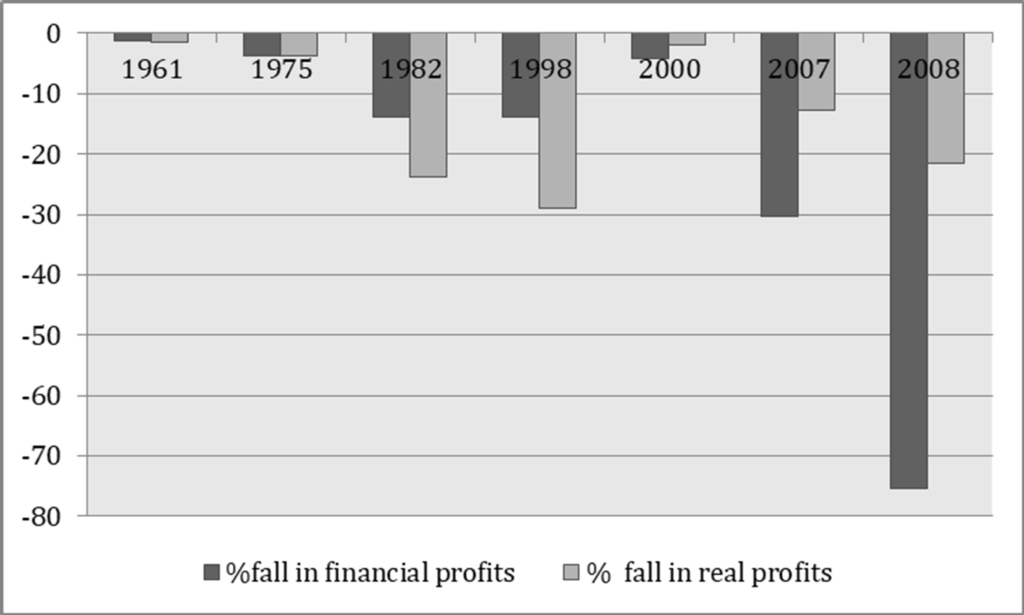

In my view, Marxist economic theory does have an answer. It relies on an objective view of the laws of motion under capitalism, in particular, changes in the profitability of productive (value-creating) capital. If profitability is low in productive sectors, capitalists try to counteract this in several ways, one of which is to invest in what Marx called fictitious capital. But financial profits still depend on the profitability of the productive sectors and if profitability falls to the point that the mass of profits or new value (wages and profits) falls, then a crisis ensues in the productive sector that flows into the financial sector. I and other Marxist scholars have provided much empirical evidence to explain recessions and, in particular, the global financial crash and the ensuing Great Recession, not as a ‘Minsky moment’ when financial stability turns into instability suddenly, but as ‘Marx moment’; when profits drop to the point where the value of means of production and labour must be devalued, including fictitious assets.

Indeed, as G Carchedi has shown (see graph below), when both financial profits and profits in the productive sector start to fall, an economic slump ensues. That’s the evidence from the post-war slumps in the US. But a financial crisis on its own (as measured by falling financial profits) does not lead to a slump if productive sector profits are still rising. see Carchedi, pages 59-62 Chapter 2 of World in Crisis.

PK view that demand creates supply

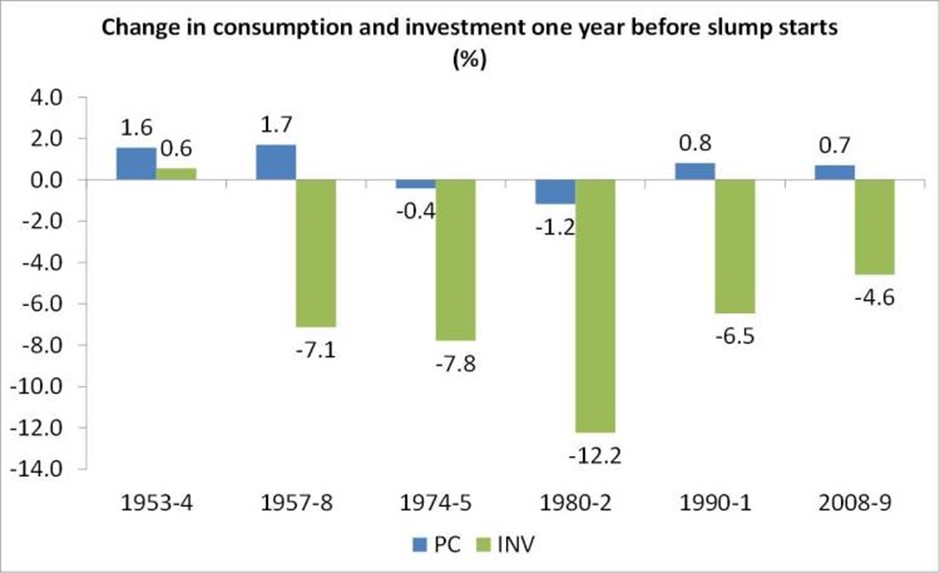

Nevertheless, Alex ploughs on with the PK view that “Demand creates supply, by driving investment. Investment then creates both savings and the capital stock while the capital stock in turn creates resources.” Again, there is no explanation of why demand slows or falls, leading to an investment collapse. “Consumption, not savings, drives investment and helps society prepare for the future” says Alex. But the empirical evidence is the opposite. In nearly every single recession in the US since 1945, it has been investment that has dived before while consumption has hardly dropped. And decisively, it is profits has led investment into slumps and out of them, not vice versa.

Alex quotes “Keynes very famously cites the “Fable of the Bees” in the General Theory. As quickly as possible, the fable tells the story of a community that outlaws luxury and finds itself much poorer now that everyone who used to work in luxury production is out of work.” Here we have the ludicrous argument offered by Keynes and the early 19th century reactionary parson Thomas Malthus before him that without rich people spending, there would be a ‘lack of demand’ and economies would go into slumps. These are soothing words to the ears of the billionaires owning the FAANGs, (apart from being empirically incorrect as many studies show the rich tend to save more than the poor, as they have done in the COVID slump).

Alternative theories of crisis

According to Alex, what’s wrong with alternative theories of crises is that they assume investment must come from savings so that consumption must be curtailed in order to allow for investment. “In the Ricardian story, which is still used today by Marxists and Austrians, the main fund for investment is savings. The assumption is that the economy has a maximum capacity that it is usually running at, and that whatever is not consumed in a given period is saved. In order to invest, savings have to come first, so ipso facto consumption has to be curtailed in order to increase investment.”

Alex reckons that Keynes trashed this view with his idea of the Paradox of Thrift. “If everyone tries to increase their savings rate, that means they are cutting their consumption rate. If their consumption rate declines, then the incomes of the people selling things to consume falls. Problem is, total output is set by consumption and investment. If investment stays constant and consumption falls, total output falls. The savings rate goes up, but only because everyone is now saving the same amount in dollar terms out of a lower income in dollar terms.”

As Alex says, PK’s Kalecki “looks at the same idea from the firm side, rather than the household side. If employers minimize costs by minimizing wages in aggregate, they wind up cannibalizing the consumption base of the economy as a whole, which eats into profits. If you go the other way, and let wages rise, the rate of profit rises right alongside.”

Paradox of profitability not a ‘Paradox of thrift’

There are two things here. It may be the view of the Austrian school that savings are needed for investment, but it is not that of Marxist economics. It is not ‘savings’ that is required for investment, but profits, or capitalist savings. Household savings are not required to kick off the capitalist accumulation process. What follows is that profits then lead investment which in turn leads to employment, incomes and finally consumption – the reverse of the PK view. Which is correct? I have already cited the evidence.

Indeed, there is not so much a ‘paradox of thrift’ Keynesian-style but a ‘paradox of profitability’, namely as capitalists strive to raise their individual profitability through investments in means of production and shed labour, they actually reduce the overall profitability of the capitalist economy and eventually provoke a crisis.

The second point is that the Kalecki theory leads to an eclectic view of crises. Sometimes they are ‘wage-led’, ie wages and consumption are too low to sustain growth and sometimes they are ‘profit-led’, ie wages are too high and profits too low to sustain growth. But neither shall the twain meet. There is no coherent theory of the causes of regular and recurring crises every 8-10 years; sometimes it is one thing and sometimes the other.

Policy conclusions

That brings me to the policy conclusions of PK, as expressed by Alex. Alex does not see the need to end the market system of production and investment. Instead, it is the job of the state to regulate and counteract the failures and inequalities of the capitalist economy. As Alex says, “this is an elaboration of the John Kenneth Galbraith position, that the state is meant to be a “countervailing power” to firms in the market. If they don’t like the social impact of the way private actors are governing markets, they’re more or less able to step in and change things. It’s impossible to say that this isn’t legitimate, because the state is one of many actors in the market, but it’s also not particularly radical to say that it is legitimate.” Yes, not very radical at all.

You see for Alex and PK, “A market is just an administrative technology that provides actors a place to coordinate. A price signal is just one of many that obtains in a well-functioning market.” Really, a ‘well-functioning’ market? Hardly supposed to be the view of PK, surely? Or maybe it is.

Attack on class theory

Alex goes on to trash a class theory of modern capitalism: “The idea that there exists a global logic to all of the contingent market governance structures arrived at through the processes above winds up dooming most mainstream analysis, but also most Marxian analysis as well. There is no underlying unified “logic” of capitalism, just a number of iterative and competing governance structures. No individual or group behavior is really commensurate with emergent structural behavior.”

Alex wants to dismiss the Marxist idea there are specific social structures based on different modes of production and classes based on those modes and structure. For him, economics is not political economy but about establishing an “administrative technology” to make capitalism work for all.

So when we get to the end of the theoretical analysis we also end up with much the same pro-capitalist view as ‘bastardised Keynesianism’ or even mainstream neoclassical economics. The policy aim that results from PK is to regulate the capitalist system and use the state to ‘countervail’ its failures in order to produce a ‘better functioning market’. But even Alex, has to admit at the end of his explanation of the ‘principles’ of PK, that “no regulatory system is ever really final, and capitalism is never really solved, the only goal is to move on to the next.” Indeed.

From the blog of Michael Roberts. The original, with all charts and hyperlinks, can be found here.